Key learnings:

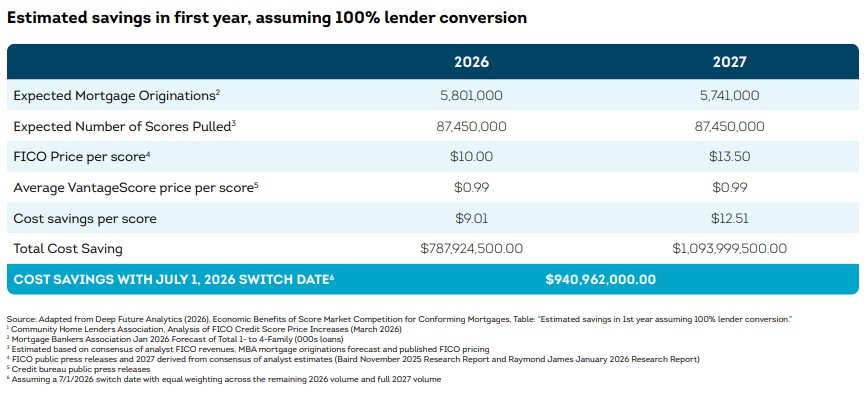

- Credit score competition, enabled by adopting VantageScore® 4.0, has the potential to unlock nearly $800M in mortgage credit cost savings in 2026 — and more than $1B annually by 2027 — driven by lower per‑score pricing at industry scale.

- These cost savings can be achieved without compromising safety and soundness; modern models built on robust trended credit data support strong underwriting performance and maintain investor confidence.

- Expanding choice and transparency in mortgage credit scores supports responsible market modernization, giving mortgage lenders greater cost certainty and flexibility to reinvest in affordability, innovation and risk management.

Disclosure:

Remember that this material is intended to provide you with helpful information and is not to be relied upon to make decisions, nor is this material intended to be or construed as legal advice. You are encouraged to consult your legal counsel for advice on your specific business operations and responsibilities under applicable law. Trademarks used in this material are the property of their respective owners and no affiliation or endorsement is implied.

How mortgage lenders can unlock $1B+ in annual mortgage credit cost savings with VantageScore® 4.0 — without compromising safety and soundness

The mortgage industry stands at a pivotal moment regarding mortgage credit scores. As policymakers, regulators and market participants evaluate the future of credit scoring in housing finance, one challenge stands out clearly: Rising credit score costs are placing increasing pressure on mortgage lenders at a time when affordability and operational efficiency matter more than ever.

New analysis shows introducing credit score competition could help achieve meaningful mortgage credit cost savings without compromising the safety, soundness and confidence that underpin the US housing finance system. VantageScore 4.0 is a next-generation credit scoring model designed to support responsible credit growth while maintaining strong, consistent risk performance across economic cycles.

Why mortgage credit scores are a growing cost challenge

Over the past several years, lenders have faced escalating costs tied to mortgage credit scores, driven largely by limited choice in the marketplace. These costs are absorbed across the industry, affecting lender margins and, ultimately, borrower affordability.

For mortgage lenders operating at scale, credit score expenses are not marginal; they’re structural. When pricing increases occur without competitive alternatives, lenders have little ability to plan, forecast or mitigate long‑term costs.

How credit score competition creates mortgage credit cost savings

Credit scores are pulled tens of millions of times each year to support mortgage originations. Even modest differences in per‑score pricing can translate into hundreds of millions of dollars in annual expense for the industry.

Introducing competition rebalances this dynamic, giving mortgage lenders:

- Greater pricing transparency

- Predictable cost structures

- Flexibility to reinvest capital elsewhere in the lending lifecycle

How competition affects credit scoring

Credit score competition does not alter underwriting discipline; it alters market dynamics. Multiple validated models operating side by side encourage pricing fairness while maintaining rigorous performance standards.

VantageScore 4.0 and the economics of mortgage credit scoring

VantageScore® 4.0 was designed to meet the needs of modern mortgage lending. Built on robust trended credit data, it provides a more dynamic view of consumer credit behavior, enabling lenders to more responsibly identify creditworthy borrowers.

Just as important, the model is available at an average price of $0.99 per score, creating a meaningful opportunity for mortgage credit cost savings at scale.

Trended data and modern credit scoring in mortgage lending

By incorporating credit behavior over time rather than relying solely on static snapshots, modern credit scoring in mortgage lending supports:

- More nuanced risk assessment

- Consistent underwriting outcomes

- Confidence across the secondary market

Estimated industry savings from credit score competition

Based on projected mortgage origination volumes and publicly available pricing data, adopting VantageScore 4.0 across the industry could unlock substantial savings.

Safety and soundness in mortgage lending remain paramount

Lower costs alone are not sufficient. Safety and soundness in mortgage lending are non‑negotiable requirements for lenders, investors and regulators.

Importantly, credit score competition does not weaken risk controls. VantageScore 4.0 is designed to deliver strong predictive performance within existing mortgage underwriting frameworks, leveraging trended credit data and maintaining high score consistency — capabilities that support reliable credit decisioning and investor confidence.

Why credit score competition does not increase risk

Competition rewards performance, not shortcuts. When models compete on predictive power, consistency and transparency, the entire housing finance system benefits.

Mortgage market modernization through credit score choice

Credit evolution is not about disruption; it’s about responsible mortgage market modernization. Introducing choice in mortgage credit scores enables the market to operate more efficiently while preserving the standards that have long supported stability.

For mortgage lenders, this means a future with:

- Lower structural costs

- More transparent pricing

- Strong alignment with regulatory expectations

Stay informed with the Monthly Credit Industry Snapshot

To track ongoing trends in credit performance, borrower behavior and market health, explore TransUnion’s Monthly Credit Industry Snapshot.