Key Takeaways:

- Canceling a credit card can hurt your credit score.

- When you cancel a credit card, there are multiple credit score factors that can be impacted.

- By how much your credit health is impacted depends on your credit history and the credit scoring model used.

- There are different credit scoring models.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Perhaps you’re wondering: Does canceling a credit card hurt my credit? It may seem counterintuitive, but closing a credit card can hurt your credit score in the short term. You may be less likely to spend if the card is gone, but without that information on your credit report, the lender has also lost insight that could help them gauge your credit worthiness, or your reliability as a borrower.

What happens if I close a credit card?

It’s important to think about the benefits and drawbacks of what closing a card would do to your overall credit health and score before you go through with a cancellation. To close a credit card, you will need to pay off your remaining balance and contact the lender. You may need to call the lender directly to close your account.

When you close a credit card account, you lose access to the card’s credit limit. If you have outstanding balances on other credit cards, you may see an impact to your credit score. Why this can happen is explained in a section below. Closing the card could also make your average age of credit shorter, and your credit mix potentially less diverse. This could also impact your credit score. By how much depends on your personal credit history.

How does closing a credit card affect your credit score?

There are many different credit scoring models, each a little different from the next, but they generally focus on similar credit score factors. The factors discussed below are based on the VantageScore® 3.0 model. Closing a credit card can affect your credit score due to a couple factors:

- Credit depth

- Credit utilization

Credit depth

Credit depth is an important factor that considers the length of credit history and your credit mix.

A long history of using credit responsibly helps lenders feel confident in your ability to continue healthy credit behaviors. Closing the credit card account affects the number of active accounts on your credit report. This could potentially lower your credit score, though usually not dramatically.

Account mix

Focuses on the different types of credit accounts you have open such as credit cards, student loans, mortgages and car loans. Lenders typically want to know that you can manage several loan products. Having a mix of revolving accounts (like credit cards) and installment accounts (such as mortgages) can help because it demonstrates your ability to carefully manage multiple financial obligations and builds your credit. If you close the only credit card account you have, it may make your credit mix less diverse.

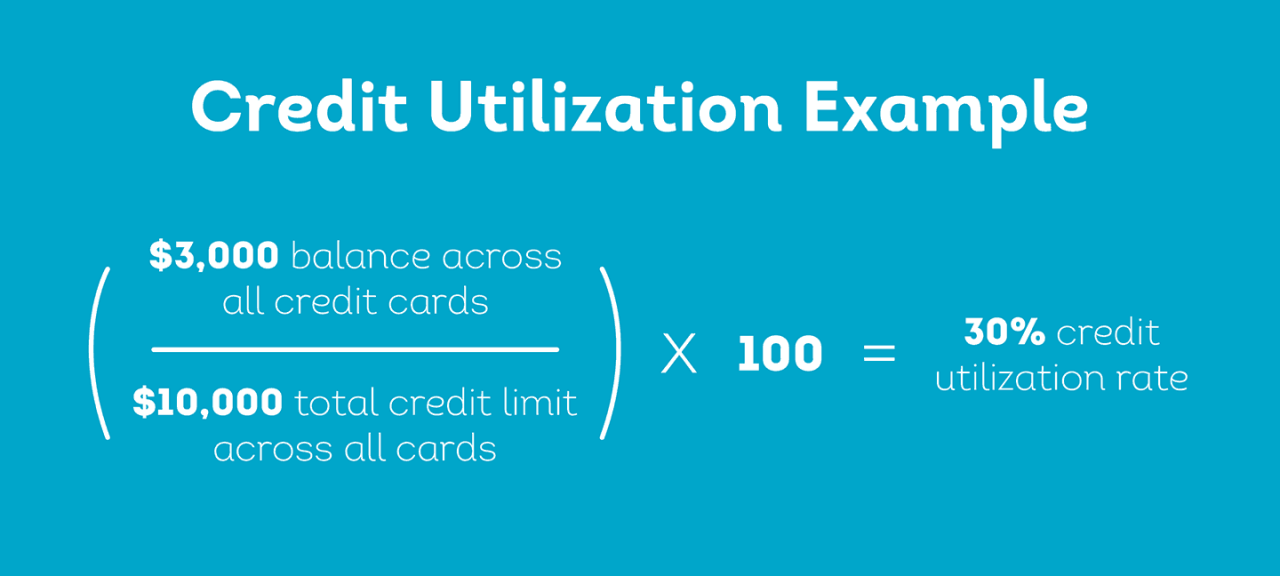

Credit utilization

Credit utilization is another factor that influences your score. Your credit utilization is the amount of debt you have compared to your total credit line available. For instance, if you have multiple credit cards with a combined credit limit of $10,000, and $3,000 in outstanding balances spread across those cards, your credit utilization is 30%. Try to keep your utilization at 30% or less if possible, meaning you’re only using up to 30% of your overall limit. However, the lower the better.

How does canceling a credit card impact your credit utilization?

When you close a credit card account, you lose access to that card’s credit limit. It may impact your credit utilization if you have balances on other credit cards. By lowering your total credit limit, your credit utilization rate would increase, which can then impact your credit health.

The impact can be more significant if you cancel a credit card with a high credit limit (i.e., $15,000). If your total credit limit decreases, you can improve your utilization by paying down balances.

Can canceling a credit card help you?

As you can see, closing out a card can impact your score given the impact on important credit score factors. However, there are certain circumstances when closing an account is a good idea. If a card issuer charges a high annual fee and you’re not using the available benefits, or if you’re tempted to overspend, it may be best to close the account. This can save you money.

Review your credit report

Canceling a credit card can impact your credit health, so it’s important to consider the decision carefully before you do so. Creating a well-thought plan may help you avoid or minimize changes to your score. Think strategically about when and how you cancel your credit card, consider all options, and choose wisely.

Before making important credit decisions, it can help to know where you stand. You can get your credit report from each of the three nationwide credit reporting agencies weekly at annualcreditreport.com.

You can also get free daily refreshes of your TransUnion credit report and credit score with TransUnion's free credit monitoring subscription. There is no credit card required to sign up. Learn more about your credit report options on our free credit report page.