Key Takeaways:

- Credit score changes are driven by changes to information in your credit report, even if they aren’t obvious.

- Changes like a higher reported credit card balance, a reported late payment or a closed account may impact your credit score.

- Checking your credit report will help you determine what caused your credit score to change.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

If you’ve checked your credit score and noticed it dropped, even though you don’t think anything changed on your credit report, it can feel confusing. While it may appear nothing has changed, there may be some less-obvious changes on your credit report that caused your credit score to go down. Let’s discover what may have happened below.

Why did my credit score go down for no reason?

The important thing to know is that credit scores don’t change for no reason. Changes in your credit report hold the key.

Your credit score is calculated based on the information in your credit report. To create your credit score, the information is broken down into different categories or factors. These factors may be weighed differently based on their importance. For instance, for the VantageScore® 3.0 credit score model, your payment history, credit depth and utilization are the most important credit score factors.

When information is updated in your credit report, your score may change as well. By how much depends on the nature of the updated information. Because information in your credit report may be updated frequently, changes that cause your score to fluctuate may not be obvious.

There are also different scoring companies that provide credit scores, and they have their own models. It’s common to see differences in scores from one model to the next. That said, if you see a big drop in your score, it’s usually triggered by something specific.

Why is my credit score going down?

To discover the cause of a credit score drop, it’s important to read through your credit report. Your knowledge of the credit score factors combined with clues in your report will help you find the answer. Below are some common reasons why your credit score might have dropped:

You have a high balance on your credit cards

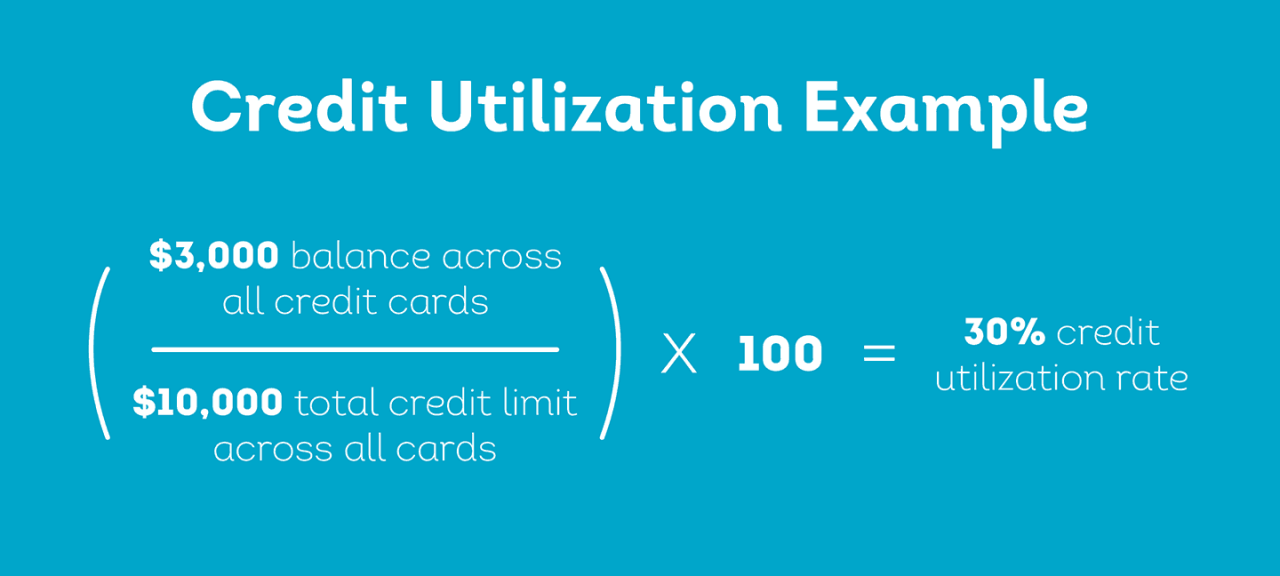

Your credit utilization, which is one of the most important credit score factors, measures how much of your available credit you’re using. If you have high credit card balances, a good goal is to get it to 30% of your total credit limit. For example, if your total credit limit across all your cards were $10,000, you’d want to keep your total balances below $3,000 to limit the negative impact on your score. Of course, getting at or close to 0% is best. Low utilization shows lenders that you are a responsible borrower and repay most or all your purchases quickly.

Did you make a large purchase on a credit card recently? It’s easy to inflate your balance with big-ticket items like home appliances, furniture and home repairs. Even if you paid it off quickly, there is a chance your lender reported this higher balance before you paid it off. Once the balance is reported as being paid off, your reported utilization should return to prior levels.

A late payment was reported

Your payment history is another important credit score factor. If you’ve recently missed a payment, it could cause a drop in your credit score. If you look at your credit reports, you should see your history of payments for each account listed. This is where you want to check if you see a sudden, significant drop in your score. Consider setting up reminders or turning on automatic payments, if possible, so you can keep up with the important payment dates for your accounts.

You closed a credit card account or paid off a loan

Closing a credit card account can affect your credit score in a couple ways. If you close one account, maybe one you haven’t used in a while, but still have a balance on other cards, it can increase your utilization.

Let’s say you have two credit cards, both with a $1,000 credit limit. One card has a $500 balance, and the other, a card you never use, has no balance. Your current utilization rate is 25% ($500/$2,000). That’s below the 30% threshold lenders like you to be at. But if you close the second card that has no balance on it, you’ll increase your utilization — up to 50%. You have to be mindful when closing credit cards for this reason.

Closing a credit card can also impact your score by changing the average age of all your accounts. Lenders like to see that you have active accounts with a long history of on-time payments. . If you close an account that’s been open for a long time, it could bring down that average. Think carefully about closing old accounts, especially if you want to limit any negative impact to your score.

You paid off an installment loan

Did you recently pay off an installment loan? Those are loans with fixed terms and payment schedules — accounts like auto loans, mortgages and student loans. Sometimes, paying off these loans may cause a score to drop slightly, which may seem counterintuitive. Just like with credit cards, closing an installment loan account with a long, positive history can impact your score. However, paying off an installment loan, this can ultimately be a good thing for your finances and you should celebrate that achievement.

You recently applied for credit

If you applied for a credit card or are shopping around for a loan, a hard inquiry may appear on your credit report, which temporarily lowers your score. Hard inquiries may happen when a lender or company reviews your report with the intent to make a lending decision. For example, applying for a credit card, mortgage or car loan can result in a hard inquiry.

If you applied for a loan, but ultimately were not approved, the inquiry will remain on your credit report. So while there may not be a new account added to your credit report, the new inquiry can still impact your credit. Hard inquiries can stay on your credit report for two years.

If you requested a credit line increase for one of your existing credit cards, it may also trigger a hard inquiry. Because this account may already appear on your report, this type of change would be easy to overlook.

Soft inquiries on your credit report do not impact your credit score. If you see a soft inquiry on your credit report, it means that you or a company checked your credit report.

Pro Tip:

Rate shopping for a loan in a short time frame can help limit the credit score impact of hard inquiries. Credit scoring models typically count all inquiries for one type of loan made in a short period of time as one inquiry.

You’re the victim of identity theft

Identity theft is more common than people may think and can impact your credit score. If fraudsters obtain your important personal information, they may be able to open credit accounts in your name, make charges and then not pay the bills as they come due. If not caught early enough, those accounts may become past due and go to collections.

This is why reading through your credit reports on a regular basis is so important. Doing so can help you identity inaccuracies, if there are any, and signs of fraud. To see if you have been a victim of identity theft, check your credit report for irregularities or things you don’t recognize.

Here are some steps you can take if you’ve been a victim of fraud include:

- Placing a credit freeze and fraud alert on your credit report

- Reporting the fraud to relevant companies and authorities

- Disputing inaccurate and fraudulent activity on your credit report

To learn how to get on the path to recovery, read the blog What to Do if Your Identity Is Stolen: Steps to Take.

Why did my credit score go down when nothing changed?

As you can see, there can be multiple answers to this question. Credit scores are calculated using specific information in your credit report. So if your credit score dropped, something in your credit report has changed. There is a lot of information on a credit report. If you’re unsure why your credit score dropped, carefully read your credit reports again. You may have to dig for some clues to account for a fluctuating credit score. You can get a free copy of your credit report at AnnualCreditReport.com.

If you’d like help reading through your credit report, we’ve created an interactive guide that explains each important section and how the information may impact your credit score.