Key Takeaways:

- Your debt-to-income ratio is one factor a lender may consider when determining if you’ll be approved for a loan, like a mortgage or auto loan.

- Your debt-to-income ratio compares your gross monthly income to your monthly debt payments.

- The lower your debt-to-income ratio, the better.

- How much emphasis lenders put on your debt-to-income ratio may vary.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

When you apply for a mortgage, car loan or credit card, lenders consider multiple factors such as your credit score and debt-to-income ratio. Your credit score is a three-digit number that reflects, in part, your history of paying back your debts. Your debt-to-income ratio (DTI), however, reflects how you’re currently managing your debt and income. Your DTI compares the monthly debt payments you owe to your monthly income. Together, these factors help lenders understand the risk you may pose as a borrower.

In this guide, you’ll learn what debt-to-income ratio is and how it’s calculated, so you can prepare your finances to shop for a house or other big purchase.

How to calculate debt-to-income ratio

Your DTI compares your monthly debt payments to your gross monthly income, which is your income before any deductions like taxes and insurance premiums. Debts for your DTI calculation may include a mortgage, car loan, student loan and the minimum payments on a credit card. Typically, your DTI calculation does not include monthly bills like utilities or subscriptions. If you’re applying for a mortgage, your lender may include your estimated future mortgage payment in your DTI calculation.

How to calculate your DTI:

- Add up all debt payments in one month

- Determine gross monthly income (your pay before deductions)

- Divide your total debt payments by your gross income

- Convert to a percentage

Note:

Make sure you include only required debt payments in your calculation. Credit card payments, auto, student, mortgage and other loans payments should be included. What typically doesn’t count as debt are flexible day-to-day expenses like utilities, gas, groceries, subscriptions, etc.

DTI calculation example:

1. Monthly debt = $2,850

- Car payment of $500

- Mortgage payment of $2,000

- Student loan payments of $250

- Minimum monthly credit card payments of $100

2. Monthly income = $5,500

3. Calculation: $2,850 / $5,500 = 0.52

4. DTI = 52%

What’s a “good” debt-to-income ratio?

To increase your chances of being approved for a loan, lenders generally like to see your DTI around 35% or lower. Of course, the lower the better. A low DTI can show you have enough room in your monthly budget to handle additional debt payments. What is considered a “good” DTI can vary between lenders and the type of loan for which you’re applying.

The types of income that lenders include in their DTI calculations may also vary. If you’re working with a lender, make sure to ask how they measure DTI so you can have a clear understanding of how to improve your odds of approval.

When is debt-to-income ratio used?

Your DTI can be considered by lenders for a variety of loans, including credit cards, auto loans and mortgages, to name a few. A high DTI may indicate your debt load is too high and it would be risky to lend you additional money. The lower your DTI, the more likely it is you’ll be seen as an eligible borrower.

Types of debt-to-income ratios

When applying for a mortgage, lenders may look at more than one type of DTI.

| Type of DTI | What it includes | When it's used |

|---|---|---|

| Front-end DTI | Housing costs only (mortgage, property taxes, homeowners insurance | Typically used to evaluate housing affordability |

| Back-end DTI | All monthly debts (mortgage, credit cards, auto loans, student loans and other loans) | Primary measure lenders use to assess overall debt load |

More on front-end ratio

If you’re applying for a mortgage, in addition to the more conventional DTI, your lender may also analyze what’s called a front-end ratio. The calculation of a front-end ratio is similar to that of DTI, but a front-end ratio tends to only include potential housing costs like your mortgage payment, property taxes and insurance. It would not include other debts you may have like a car or personal loan.

To find your front-end ratio, add up monthly costs related to your regular mortgage payments and divide by your gross monthly income.

For example:

- Monthly mortgage payment of $1,700 (including escrowed taxes and home insurance)

- Gross monthly income of $5,000

Front-end ratio calculation:

- $1,700 / $5,000 = .34

- Front-end ratio = 34%

Does my debt-to-income ratio affect my credit score?

Your DTI ratio isn’t used in credit score calculations. However, aspects of your credit health can be intertwined with your DTI.

For example, carrying large balances on your credit card accounts can have a negative impact on your credit score, since your credit utilization rate is an important credit score factor. At the same time, if those high balances cause your minimum monthly payments to increase, this could impact your DTI. In short: Your personal finances and credit health are closely related, but your DTI doesn’t directly impact your credit heath.

DTI and buying a home

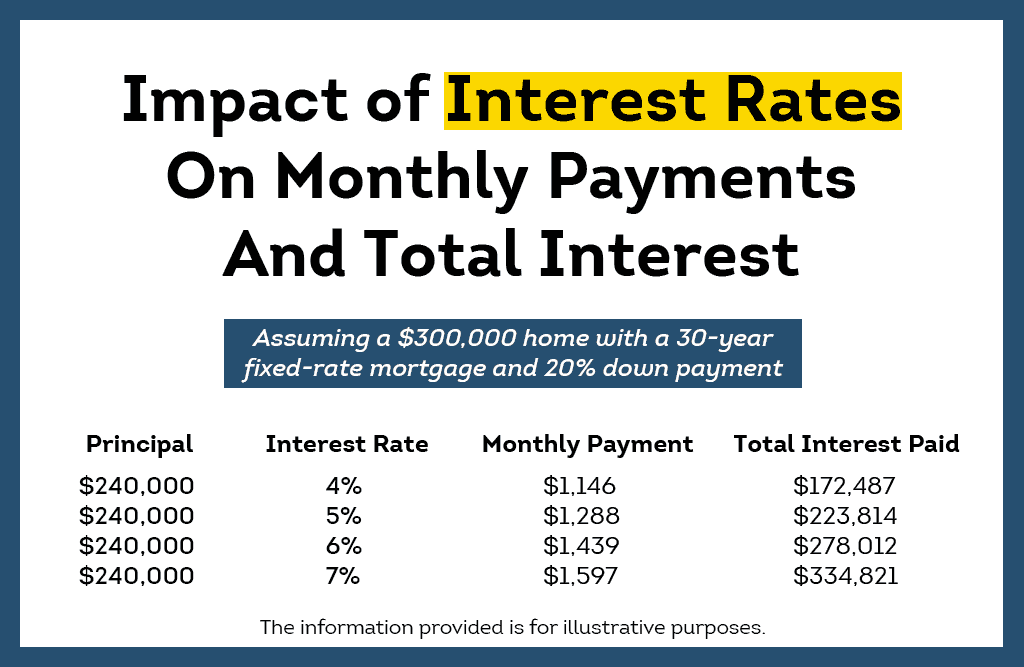

Your DTI is one of multiple factors lenders will look at to determine if you’re approved for a mortgage, along with deciding the terms of that loan. Other mortgage approval factors can include your credit score, employment and income verification and down payment requirements. How much importance is put on each of these factors can vary by lender. Working to improve your DTI and building healthy credit may help you secure a loan with a lower interest rate. Even a modest change in the interest rate of your mortgage can have big impact on the total amount you pay over the life of the loan.

Use free tools to build your confidence

Taking out a loan can require a lot of preparation and communication. From gathering financial documents to filling out applications and discussing options with lenders, there’s a lot that goes into it. The earlier you prepare, the easier the process can be.

As you get started, it’s a good idea to read your credit reports and gain an understanding of where your credit health is at. Read through your credit report and make sure everything is accurate and up to date. You can get free weekly credit reports at annualcreditreport.com.

You can see useful loan tools on TransUnion’s tools and calculators page. If you’re interested in reviewing home affordability options, you can explore TransUnion’s Mortgage Calculator tool. You can use it to help estimate monthly payments based on your home price, down payment and interest rate, among other factors.

FAQs

Your DTI is influenced by two main factors: your existing monthly debt and your monthly gross income. Reducing balances lowers your monthly debt obligations, while higher income improves the ratio from the other side. Avoiding new debt while you’re working to improve your DTI can also help you make steady progress over time.

Rent is typically not included in standard debt-to-income ratio calculations. DTI usually focuses on recurring debt obligations like loans and credit cards. For some lending decisions, like mortgages, lenders may still consider your rent payments as part of your overall financial picture. Even if it’s not formally part of the DTI calculation, it can give them additional information about your financial situation.

Front-end and back-end debt-to-income ratios look at different parts of your finances. Front-end DTI measures only your housing costs, such as your mortgage, property taxes and homeowners insurance. Back-end DTI includes all your monthly debts — mortgage payments, credit cards, auto loans and other loans.

Yes, student loans are typically included in your debt-to-income ratio. Lenders usually consider your required monthly payment when calculating DTI.