Key Takeaways:

- There’s no fixed timeline for rebuilding credit — it takes time and consistent good habits.

- Negative marks on your credit don’t last forever.

- Review your credit report so you know where you stand.

- Use credit score factors as a guide to address problem areas for your individual credit profile.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

It can be disheartening to see your credit score drop after a financial setback. Whether you missed payments, made the hard choice to file for bankruptcy or faced something else entirely, these kinds of disruptions can result in a hit to your credit health. But with a plan, adhering to healthy financial habits and a dose of patience, you can rebuild your credit. By improving your overall financial picture, your credit will follow over time.

How long does it take to raise your credit score?

Your credit scores are calculated using information in your credit report. As information is added, removed or updated on your credit report, it can then change your credit score. Lenders tend to provide updates once a month.

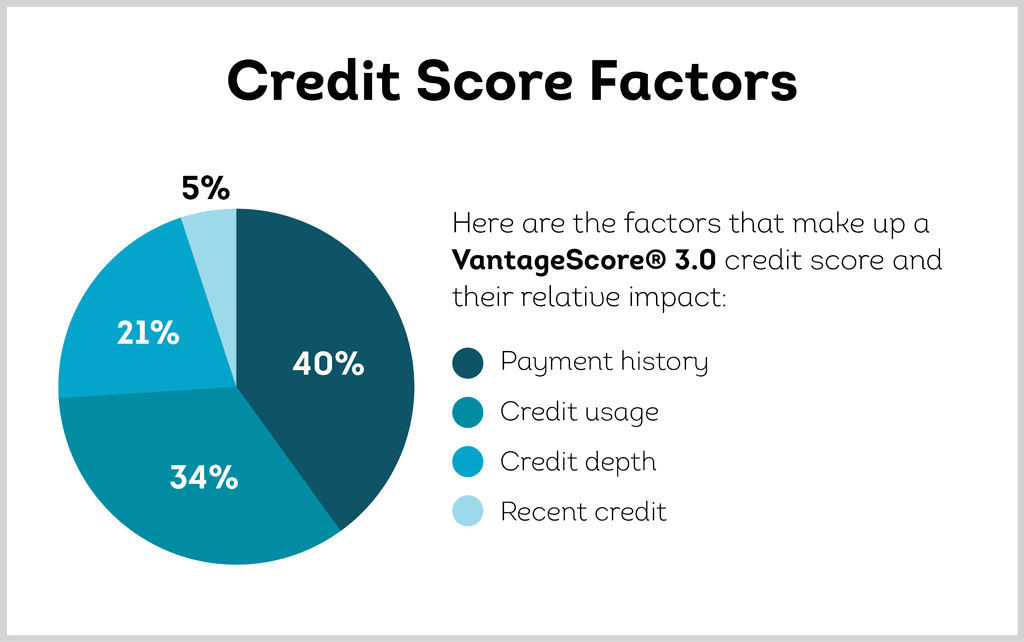

Understanding credit score factors can help you make more informed decisions as you work to rebuild your credit health and make better credit choices. There are different credit score models, but in general they tend to use similar factors to calculate credit scores.

Maybe the thing preventing your score from being where you want it to be is that you’re carrying a relatively high amount of revolving debt. If that’s the case, you’d want to do your best to pay down your credit card debt to improve your credit utilization.

Or, it could be that you missed a payment or two. A missed payment will fall off your credit report in seven years. While you can’t get rid of missed payments on your credit report if they are accurate, making strides to be sure you make all your payments on time can help you build a healthy credit history going forward. That may mean setting up automatic payments if possible. You want to make sure you have enough money in the bank account you use to cover the automatic payments. If your funds are insufficient, it could result in a missed payment.

Everyone’s credit history is different, so how credit scores respond to changes in credit reports will vary. With continued healthy habits, you should see your credit health improve over time.

9 ways to rebuild credit

Knowing the credit score factors and credit score ranges can help you set goals as you start rebuilding your credit. Patience is key since healthy credit is built on a foundation of consistent, long-term habits. But there are still some things you can do to get going in the right direction. Here are nine tips to help you rebuild your credit:

1. Evaluate your credit

Before you can rebuild your credit, you need to know where you stand. That’s why regularly reviewing your credit report is essential. You can get a free copy of your credit report from each of the three nationwide credit reporting bureaus at annualcreditreport.com. You can see additional credit report options from TransUnion, which includes daily refreshes of your TransUnion credit report, on TransUnion’s free credit report page.

The information in your credit report tends to update every 30 days, depending on the lender, so you may not need to check it every week.

2. Dispute inaccuracies on your credit report

Your credit report should be an accurate picture of your credit history. After requesting your credit report, be sure to carefully review the information within it. If you believe there is an inaccuracy in your credit report, you can file a dispute. This is easy to do through TransUnion’s online dispute process. But note that you can’t dispute items simply because they are negative. Many negative items on your credit report, like missed payments, collections and charge offs, will no longer appear on your credit report after seven years.

3. Make a budget

As you rebuild your finances, you’ll want to create a budget that works for you. A budget provides much-needed visibility into your cash flow so you can build a financial plan that’s realistic and matches your needs.

Be sure your plan allows you to pay at least the minimum amount due on revolving accounts, like credit cards, but the more of your balance that you can pay off the better. Paying at least the minimum can help you avoid late payments and keep your accounts in good standing. Of course, pay off the entire balance of each credit card if you can. Your budget should help you keep your spending in line with your goals.

Three budgeting tips

- Choose things that you care about to spend money on and cut back on things you care less about.

- Set attainable, specific goals and celebrate your success along the way.

- Try saving a small chunk from each pay period to establish an emergency fund.

4. Make on-time payments

Making on-time payments is one of the most important credit score factors. If you’re unable to make your credit card payments, reach out to your lenders to explain your situation. You can find their contact information on your credit report or most recent bill.

You can ask your lenders whether they offer hardship or forbearance plans. Not all lenders offer these plans, but if you’re in danger of missing a payment with any company, talking to them as early as possible is a good idea.

5. Reduce your credit utilization

Your credit utilization rate is a calculation that shows how much credit you’re using compared to what you have available. To limit the negative impact to your credit, you generally want to keep your credit utilization rate at 30% or less, but the lower the better. For example, if you have $10,000 in available credit, and you’re using $3,000 of it, your credit utilization rate would be 30%.

If you’re able to significantly lower your utilization rate, you may see it reflected the next time your lender reports the information, and your credit report is updated. That may lead to an improvement in your credit score.

6. Use your credit cards wisely

It may seem counterintuitive, but your current credit card can be a tool to help rebuild your credit. An active credit card account in good standing with a long history of on-time payments can reflect a positive credit history. Getting rid of your credit cards isn’t always the answer to a bad credit score. In fact, closing down accounts may hurt your score.

You need to weigh the positive and negative aspects of keeping a card open to be sure you’re making the financially healthy choice. If keeping a credit card open may cause you to spend more money and potentially miss payments, then it may be worth closing despite a potential impact to your credit health.

7. Consider a secured credit card

A secured credit card can be helpful to people with a limited credit history or those looking to rebuild their credit. With a standard credit card, if you’re approved, you’re given a set credit limit. For a secured credit card, you need to make a deposit which then becomes your credit card limit. If you deposit $500, your credit card limit is then $500.

The deposit is considered collateral, which is why it is typically easier to be approved for a secured card than a traditional credit card. Lenders will report the activity of your secured credit card account to credit reporting agencies, which can help you rebuild your credit history.

8. Look into credit builder loans

Similar to a secured credit card, credit builder loans can help people who are new to credit or are looking to rebuild their credit. When you take out a credit builder loan, you don’t receive money from the lender, rather the lender puts your monthly payments into a savings account. Your payments are a mix of interest and principal. The interest is collected by the lender, while the principal is deposited into the savings account. Essentially, the interest acts as the cost of the credit builder loan.

When you’ve made all your payments, you will then have access to the savings account. Your payment history is reported to one or more of the credit reporting agencies, which can help you build a healthy credit history.

Pro Tip:

While credit cards, secured cards and credit builder loans can help you build credit, try to limit new credit applications if you’re looking to build credit, especially if you are planning a major purchase in the near future. Credit applications can result in a hard inquiry, which can impact your credit score.

9. Become an authorized user

If you have a spouse or trusted family member with a credit card account in good standing, becoming an authorized user may help you improve your credit. As an authorized user, your credit report will reflect the positive history of the credit card account if the credit card issuer reports the account to one or more of the credit reporting agencies.

But note that the primary cardholder is ultimately responsible for the account. So, if they miss a payment or struggle with a high balance, it could have a negative effect on your credit as well. This is why it’s important to do this with someone you trust who is financially responsible.

Not all credit card issuers report account information to credit reporting agencies for authorized users. You can ask the primary cardholder to reach out to the card issuer to confirm prior to adding you on the account.

How long does it take to rebuild credit?

There’s no definitive answer for how long it takes to rebuild credit. It doesn’t happen overnight. Time and consistent good habits will help you achieve your credit goals. How long it will take you to build your credit to where you want it to be depends on your individual credit health and long-term habits. A good credit score based on the VantageScore® 3.0 model falls in the range of 661 – 780, but what is considered a good score can vary depending on the credit scoring model.

Remember: The path to a healthy financial future is a marathon, not a sprint. There may be setbacks along the way, but if you stick with your plan and prioritize good habits, you’ll be able to reach your credit goals.