Key Takeaways:

- If you don’t pay your credit card statement balance in full each month, you may be paying high interest rates on those outstanding balances.

- You want to document your debt, create a budget and establish a goal to help you get started.

- Two popular strategies to pay off debt include the avalanche and snowball methods — each have their own pros and cons.

- There is no true best way to pay down debt; create a plan that works best for your personal situation.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Credit card debt can feel like a weight that hangs over you with every financial decision you make. Having a plan can help lift that weight and give you confidence that you can achieve a healthier financial future. Let’s explore what credit card debt is and some potential strategies to pay it off:

Understanding credit card debt

Credit card debt can be particularly burdensome on your financial health because of the high interest rates. When you compare credit cards to other types of credit, like mortgages and auto loans, credit cards typically have interest rates that are significantly higher.

If you pay off your credit card statement balances each month, you won’t be charged interest. But if your balances rise to a point where you’re unable to pay off every card each month, interest will accrue and your debt can become expensive over time. This is why, if you’re struggling with credit card debt, it’s important to come up with a plan to pay down those balances as quickly as you can.

Strategies to pay off credit card debt

There are multiple strategies to pay off credit card debt. What’s important is finding the right strategy for you and your financial situation. Below are some suggestions that you can use to get started.

1. Stop using your credit cards

If possible, you’ll want to cut off the source of the problem. Stick to cash or a debit card while you are paying off credit card debt, if you can. This ensures that you’re only paying down the debt, not adding to it.

Using only cash or a debit card can help you:

- Avoid adding to your balance

- Focus on reducing what you owe

- Make progress faster

2. Know where you stand

You likely have a good idea of how many credit cards you have and where you bank. Start by gathering details about your cards, including the following information:

- Current balance

- Interest rate

- Minimum payment

But if you’re unsure, your credit report can be a good place to start.

You can get free weekly credit reports at AnnualCreditReport.com. Your credit report will show, among other information, your open and active credit accounts. You can use your credit reports to gather information about the status of your accounts, their payment history and your reported balances.

Lenders tend to provide updates to credit reporting agencies once a month, so if you know you paid down a balance and it isn’t yet reflected in your credit report, your lender may not have yet provided that update. Also, lenders can choose to report to one, two or all three nationwide credit reporting agencies. So, it can be a good idea to check all your credit reports for a comprehensive look at your credit.

Your credit reports offer a big picture look at your credit, but your individual lenders or banks will be the best place to find the most up-to-date information about your individual accounts. As you gather information, that can help you create a strategy to pay down your credit card debt. Details like your current balance, interest rate and minimum payment can help.

3. Create a budget

A budget is going to be the backbone of your plan. You’re likely going to have to cut expenses and allocate those savings to pay down your debt. But you’re not going to know what expenses you can cut without creating a budget.

Many people know fairly accurately how much money they bring in each month, but things can get fuzzy when it comes to what goes out. There are many free and paid budgeting apps you can consider. Your bank may even offer a tool that can help you track your money. Pay close attention to expenses. Of course, cutting things like housing and transportation can be difficult, but are there any other big, monthly costs you can cut from your budget? Little things add up, but you’ll gain more traction quickly by looking at your biggest expenses first and working down. Here are some questions to ask as you make your budget:

- What big expenses bring you the least amount of personal value?

- Are there free alternatives to services you’re currently using?

- Are there products you use or routines you have that have less expensive options?

What you spend money on can be considered a reflection of what you value. Just because you want to cut back, doesn’t mean you have to cut completely. Cutting expenses isn’t about deprivation, but realigning your spending with what you truly value. However, you may need to sacrifice some things now for future financial relief.

Once you’ve identified areas where you can save money, you then have to allocate those savings toward paying down your debt. If you save money in one category, you don’t want to then accidentally spend it in another. This is why having a specific plan you can follow will help tremendously.

Pro Tip:

A popular budgeting strategy is called the 50/30/20 budget, which allocates 50% of your budget for needs, 30% for wants and 20% for savings. You can use TransUnion’s 50/30/30 budget calculator to help you create your own budget.

4. Choose your debt payoff strategy

Two popular debt payoff strategies are the avalanche and snowball methods. One is mathematically focused and would technically, if followed perfectly, save the most money. The other is more psychological and motivation-based, which can also yield great results. You should choose the one you think will be best for you and your financial situation. Let’s break down each:

The avalanche method

- List all credit cards in order by interest rate from highest to lowest.

- Make minimum payments on all credit cards.

- Put extra money toward the credit card with the highest interest rate first.

- When that card is paid off, move on to the card with the next highest interest rate.

Generally, the higher the card’s interest rate, the more money you're charged on unpaid balances. With the avalanche method, because you’re focusing on the highest interest rate cards first, you would save the most money on interest payments over time. However, progress can feel slow at first, especially if credit cards with the highest interest rates also have large balances.

The snowball method

- List all credit card accounts by their outstanding balance from lowest to highest.

- Make minimum payments on all credit cards.

- Put extra money toward the credit card with the smallest balance first.

- Once that card is paid off, move on to the card with the next smallest balance.

The snowball method provides some quick wins. Paying off a balance, even if it’s small, can be motivating. Some people may be more likely to stay on track if you can consistently keep your motivation high. But because you’re determining your payback strategy on balances instead of interest rates, you could pay more in interest payments over time. Remember, the higher the interest rate, the more you’re paying to maintain that debt.

Important Note:

The reason you want to make all the minimum payments across your credit cards is because this will keep your credit card accounts current. If you don’t make the minimum payment, your lender may consider it a late payment. Your payment history is an important credit score factor and failing to make a payment can have a significant negative impact on your credit score.

5. Create a goal

You can put “create a goal” at any number on this list — just be sure to do it before you get started. You need to have some way of tracking your progress and something to work toward. And a goal should be specific. Saying, “I want to pay down my credit card balances” is a good start, but it lacks enough specificity to be motivating. “I am going to pay off $1,000 in the next 10 months” provides more direction. Now you know exactly what you need to do.

$1,000/10 months = $100 per month

Your goal can be more aggressive or less depending on your finances, but now you know exactly how much you need to cut from your expenses and allocate to your debt each month. In this case, you would use the $100 to pay any minimum payments, then take the rest and apply it to the credit card on your list, depending on the strategy you’re using.

Should you use a loan to pay off credit card debt?

Some people consider using a personal loan or balance transfer credit card to help pay off credit card debt. This can help save money on interest charges if the debt is paid back efficiently. When you take out a new loan to pay off credit cards, you’re essentially transferring the credit card debt to the new loan or credit card.

For a balance transfer credit card, you will typically have a promotional period of a low or 0% interest rate that can give you time to pay down the debt. Meanwhile, a personal loan is an installment loan, meaning you borrow a set amount and repay it over a fixed period with interest. Personal loans typically have lower interest rates than credit cards, which is why it can be useful for consolidating high-interest debt.

For both types of credit, you have to consider whether the terms of the new loan or credit card will work for your budget. Just as important, you need to make sure that you don’t increase your debt on your now clear credit card lines. An easy trap to fall into is seeing balances on credit cards zeroed out and then using them and yet again building up credit card debt. That would increase your overall debt, rendering the personal loan or balance transfer as a short-term fix to a bigger problem.

How paying down credit card debt affects your credit health

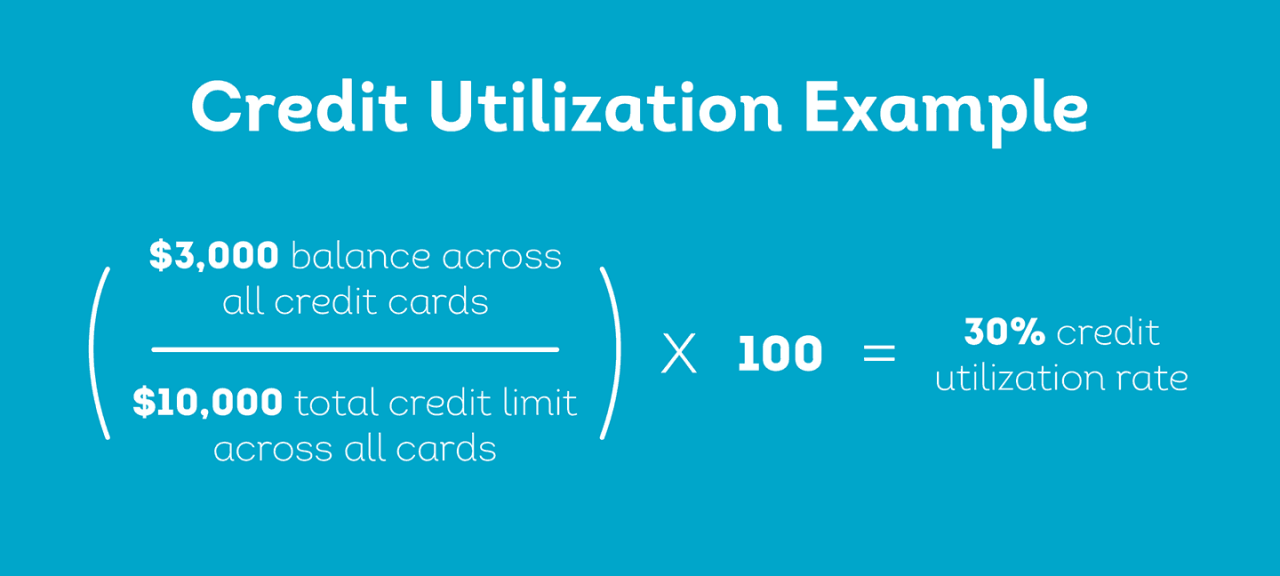

As brought up earlier, missed payments are an important credit score factor, so at least making the minimum payment on all credit cards is necessary no matter which strategy you use. Another important factor is credit utilization.

Credit utilization measures how much of your available credit limit you’re using. The lower your credit utilization, the better it is for your credit health. Popular advice is to have a goal of 30% utilization, but the lower the better. As you pay down your credit card debt, you should see your credit health improve.

As you pay off your credit cards, think carefully about whether you should leave the account open or cancel the credit card. When you cancel a credit card, it can affect the depth of your credit history. Credit scoring models favor older, active accounts. Closing a longstanding account can negatively impact your credit health. However, your ultimate goal is to save money and pay off debt, so if you’re tempted to overspend by leaving the credit card open, it may be best to close the account.

What’s the fastest way to become debt-free?

There is no true fastest way to become debt-free. As with all things related to credit and financial health, to be successful at paying down debt, you need a combination of a solid plan, sound financial habits and time. If you know where you stand, create a goal and a budget and implement a strategy that you think will work for you, it will go a long way to a healthier financial future. Make sure to give yourself some grace. Setbacks can happen, but do your best to get back on track.

For additional help, you can use TransUnion’s Credit Card Payoff Calculator tool. You can use it to test different payments and timelines.

FAQs

This is known as the snowball method. Some people find that paying off small balances can give them quick wins and provide motivation to keep going. However, the avalanche method, which prioritizes higher-interest-rate cards first, can help you pay less in interest. You should pick the method you think will help you pay down your debt efficiently.

First, you want to have a list of all your credit cards and the important information for each account, like their balances, interest rates and minimum payment requirements. Then you will want to order them according to the strategy that works best for you. Make at least the minimum payment on all your credit card accounts, then allocate extra money to the first credit card account on your list, however you feel it’s best to order them. After the first credit card is paid off, continue down the list until all the cards are paid off.

There is no one true fastest way to get rid of credit card debt. Everyone’s financial situation is different and you should create a plan that works best for you. How fast you’re able to pay down credit card debt is going to depend on the amount of debt you have, how much money you’re able to allocate to paying down the debt (this can be determined by a budget you set and expenses you cut) and your ability to stay on track with your payoff strategy.

Credit card balance transfer cards are a popular strategy to help pay off high interest credit card debt. However, if you’re unable to pay off the debt before the promotional period ends, you may still be charged interest on the unpaid balance. Additionally, if you’re not strict with the budget you set, there is a risk of adding more debt if your spending isn’t under control.