Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

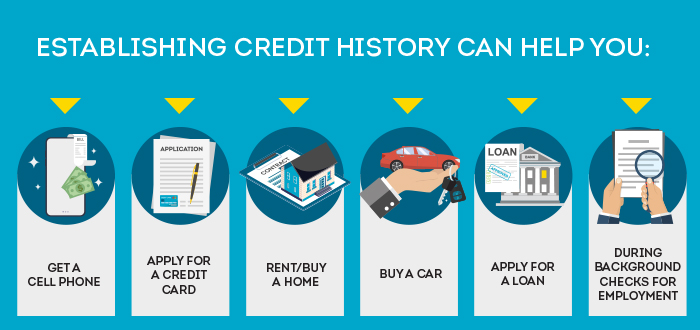

If you’re new to the United States, you’ve probably got a lot on your mind. There’s plenty to do to get settled, including getting your finances in order. Establishing and building credit is an important step when it comes to your financial goals. It will help you participate in the marketplace, whether you want to buy or rent a home, purchase a car or start planning for your future.

Most credit histories from other countries don’t transfer to the United States, which means you’ll likely need to build credit from scratch. You may be wondering: How long does it take to build credit? The truth is, it takes time, and there aren’t shortcuts to building credit. Be wary of anyone promising a quick fix.

Common credit questions for non-citizens

Credit touches a lot of different aspects of our lives. Establishing and building your credit history is a way to tell the story of your financial health and responsibility. It will likely play a part in different financial opportunities in your future, including homeownership, business loans and personal loans.

Building credit takes time. It doesn’t happen overnight. While we can’t put an exact timeline on how long it may take, healthy habits like paying bills on time will contribute positively to your credit file.

You might. If you’ve never applied for credit, it’s likely you don’t have a credit file yet. But there are two ways you can check if you do have a credit report.

If you have a Social Security Number (SSN), you can request your TransUnion credit report online through annualcreditreport.com or the TransUnion Service Center.

If you don’t have a SSN, you may still have a credit file with TransUnion. You can contact us directly and our agents can help you check.

Consistently reviewing your credit report is one of the foundations of healthy credit. It’s a good way to see how your habits affect your credit history over time. You can learn more about how to read the information in your credit report through our interactive tool.

Credit scores are calculated based on the information in your credit report. You can think of a credit score as a snapshot of your credit history at one moment in time. If you have no credit history, you may not have a credit score. For more information, learn more about how credit scoring works in the U.S.

Credit history established in other countries typically doesn’t transfer to the United States. However, there are some lenders or credit services that may allow you to use credit history from your home country to help you apply for a U.S. credit product or loan. Please note that this often only apply to a limited number of countries and may not apply to you.

How to start building credit

As you start your credit-building journey, we’re here to help you along the way. In fact, the following tips can be used by anyone looking to start building credit.

Determine if you have a SSN or ITIN

First, it’s important to know whether or not you have a Social Security number. If you don’t have one, you may have an Individual Taxpayer Identification Number (ITIN). ITINs are issued to people who need a U.S. taxpayer number but aren’t eligible for a SSN.

Your access to certain credit products or opening bank accounts may depend on whether you have a SSN or ITIN.

Open a bank account

Credit cards can be a great option for building credit, but some may require a U.S. checking or savings account in order to get one. Opening an account with a bank or credit union can be a good first step in establishing your financial and credit history.

Get started with a credit card

Since you’re starting from scratch, you may not be able to get a standard credit card, which might require an established credit history or SSN for approval. However, there are options – it’s just a matter of finding the one that may be best for you. Choosing the right card also depends on your personal spending habits. Here are a few additional options:

Consider a secured credit card: If you’re not approved for a standard credit card, a secured credit card may be a good option. This requires an upfront deposit, which acts like the card’s credit limit. You can’t use the deposit to pay off the outstanding balance, and will still need to pay the balance in full. If you don’t, the lender will use the deposit to pay it off. In the future, if you get a standard card or close the secured card’s account, the issuer will refund your deposit amount.

Become an authorized user on a credit card: If you have a trusted friend or family member with good credit history, they can add you as an authorized user on one of their credit cards. This means you’ll get your own card and can start building credit by making on-time balance payments. Over time, this will help you build a credit history that reflects responsible credit card usage. But you won’t be the primary account holder who is responsible for all charges. That person will be able to see your card usage and your activity, like making payments on time. Your usage, whether positive or negative, will also affect their credit file.

Build healthy credit habits

No matter what credit card you go with, consistently paying the monthly statement on time can help positively impact your credit history. Your payment history is an important factor when it comes to building credit and your credit score. It shows how you’re managing your finances. It’s also a good habit to keep your card balance as low as possible. Your credit utilization rate, or how much of your available credit line you're using, is another important credit score factor.

Building credit into the future

There’s no shortcut to building credit. It takes time, but we’re here to help you along the way. Getting started now and establishing healthy habits early will help you build a solid credit history.

Over time, your credit file will tell a consistent story of financial responsibility, serving you well now and into the future, whatever your goals are. Learn more about what’s considered a good credit score in our blog post.