Key Takeaways:

- Credit scores are calculated using information in your credit reports.

- Your score may move up or down depending on the type of information that was added, changed or removed from your credit report.

- Products that may help build credit include secured credit cards and credit builder loans.

- To help build your credit, you can also consider becoming an authorized user on a trusted family member or friend’s credit card account or see if your landlord reports rent payments to credit reporting agencies.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

You may have some big financial goals, and a healthy credit history is a way to help you achieve them. But how do you build that credit history from scratch? How you start building credit is going to depend on your personal and financial situation. There is no single “best” path for anyone.

Read on to learn the basics about how credit scoring works and ways to build credit:

How credit works

Your credit scores are calculated using certain account information from your credit reports. Information is added to your credit report when companies like banks, credit unions and even some landlords report account activity to credit reporting agencies. Information they report can include your payment history, last reported balance and the account’s status.

Your score may move up or down depending on the type of information that was added, changed or removed from your credit report. Information related to your accounts can impact your credit score, but your personal information isn’t included in credit score calculations.

What is the starting credit score?

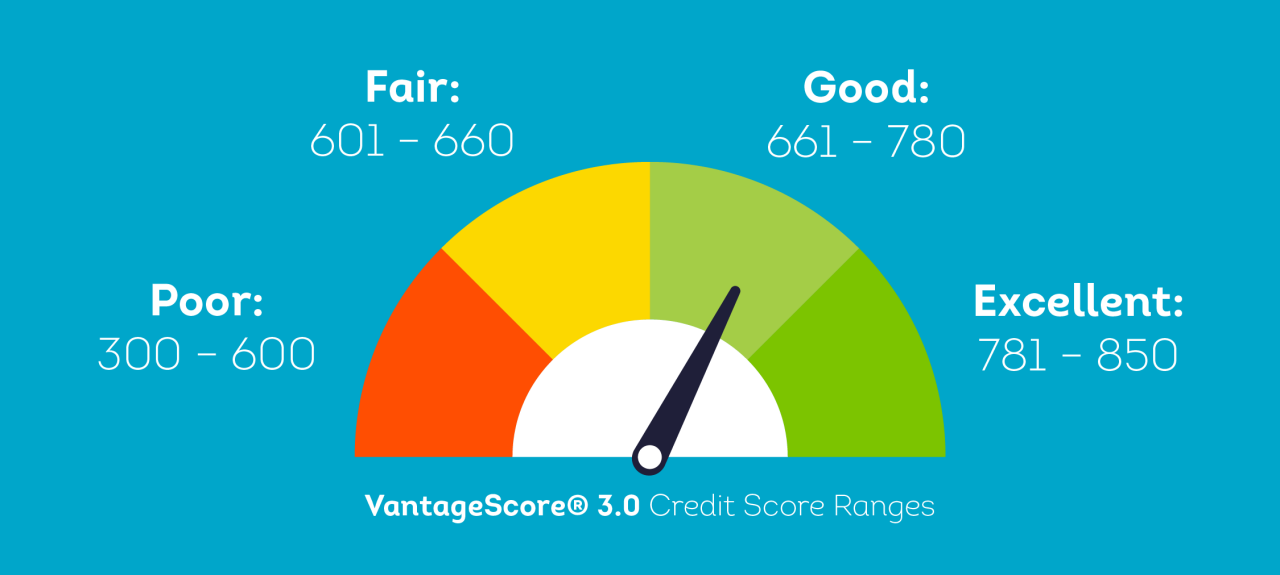

There is no standard starting credit score. If you have no credit history, you simply won’t have a score at all. The credit scores for two popular credit scoring companies, VantageScore® and FICO®, range from 300 – 850.

Once you start building credit, whether it be from your first credit card, loan or other credit product, you don’t necessarily start at the bottom. You’ll typically establish a score once the lender reports the account to the credit reporting agencies (Equifax®, Experian® and TransUnion®). It may take several months for a credit score to be established after you open a credit account. How long it takes can depend on the credit scoring model.

What is your credit score?

Your credit score reflects how well you’ve managed credit. There are different credit scoring models used by the credit reporting agencies, so your credit score can be different depending on which model is used to produce your score. However, credit score factors tend to be similar between credit scoring models. Though how much importance each model places on certain factors may be different. For example, below is a breakdown of the VantageScore® 3.0 credit score factors:

As information is added, removed or changed on your credit report, you may see an impact on your credit score. Knowing the credit score factors can help you make better decisions as you manage credit.

Ways to build credit

A healthy credit history can help you achieve the financial opportunities you deserve, like getting approved or securing better terms and rates for life’s major purchases, like a car or home. Below are some ways you can start building credit.

Ways to build healthy credit

Keep credit card balances low

Reduce credit utilization

Demonstrate positive payment history

Monitor your credit reports

Become an authorized user

Use a credit builder loan

Become an authorized user

If you have limited or no credit history, becoming an authorized user on an already-existing credit card account held by someone you trust, like a spouse or parent, is one way to help build credit. Becoming an authorized user builds your credit history because the account’s history may appear on the authorized user’s credit report. Credit scoring models may use that information in their credit score calculations. To become an authorized user, the primary cardholder will need to contact the company to add you to the account. The primary cardholder is responsible for the activity on the account, even if purchases are from the authorized user’s card.

It’s important to partner with someone who has a positive history on this account. It’s not just positive information that is reported, but potentially adverse information, like missed payments, as well. The primary cardholder should check with their lender to be sure they report account activity for authorized users, since not all lenders do. As an authorized user, you will have a card in your name and can make purchases. How and when will you pay back any charges? Do you know the credit limit of the account and how much you can use at any given time? This is a financial relationship, so you should both be open and clearly communicate about how you will manage your activity with the card.

Credit cards for building credit

Credit cards are a popular option for building credit, and you may be approved for one even if you have a limited credit history. When you open a credit card account, your lender will report your account activity to the credit reporting agencies. You’ll see important account information, like your reported balance and payment history. Lenders tend to provide updates at least once a month. If you're making your payments on time and keeping your balances low, you should see the positive behavior reflected in your credit report and score.

There are plenty of cards to choose from. It’s important to choose the right credit card that matches your goals and financial situation. Secured credit cards are a worthwhile option to explore. Instead of a traditional credit limit, secured credit cards require a down payment. That down payment typically becomes your credit limit, meaning you can spend up to that amount at any given time. Activity on a secured card is reported to credit reporting agencies, which can help build credit.

You can get your down payment refunded if you cancel the card or upgrade to a regular credit card as long as you’re up to date on your payments. Secured credit card terms can vary by issuer, so be sure to fully understand how your card works before applying.

Also, some lenders offer student credit cards specifically for college students. They’re essentially regular credit cards but typically have higher rates of approval for people with a limited credit history. Like all credit card applications, you will likely need to provide some proof of income, even if it’s a student job, to be approved. If you have no or limited credit history, it may mean you’ll have a lower credit limit. But your credit limit can usually be raised after some time if your account remains in good standing and you continue to make payments on time consistently.

Use a co-signer

If you have no credit history or limited credit history, it may be tougher to be approved for certain loans. If you’re having trouble getting approved for a loan you need, you may be able to use a co-signer. Ideally, you should ask someone who has a healthy credit history to help your chances for approval. Your loan information will be reported to credit reporting agencies, which can help build your credit history. The loan information will also be reported on the co-signer's credit report as well. A co-signer agrees to take full responsibility for paying back the loan, along with you, the primary borrower. Because this takes tremendous trust in your ability to pay back the loan, co-signers tend to be a family member.H3: See if your rent payments are reported

Renting can impact your credit if your landlord is reporting your monthly payments to the credit reporting agencies. If they are reporting, consistently making on-time payments can help you build a healthy credit history.

If you’re not sure, you can ask your landlord whether they report rent payments to credit reporting agencies. If they’re not, you can request they do so, since it could benefit both of you. There are products that can benefit your credit history by helping monthly rent payments get reported to credit reporting agencies. There are some rent reporting services that landlords need to apply for and manage, but there are other services you can apply for yourself.

There are options for you to report your own rent. Here are some things to consider before you start reporting your own rent:

- Make sure you can pay rent on time

- Make sure your rent is added to your credit report so it is available for use in credit score calculations

- Understand if only positive payments or your full payment history will be reported

- Understand if fees are charged for self-reporting rent

- Know the cancellation policy

- Know that not all credit scoring models may consider rent payments in score calculations

Take out a credit builder loan

A credit builder loan can be a useful tool for building credit history, but it can come with a cost. With a typical personal loan, the lender would send the funds directly to you to use as needed. With many credit builder loans, your lender sends the funds into a bank account to hold until the end of the term of the loan. You would make regular monthly payments like a regular loan, but when the loan term is over, the bank releases the funds to you.

Instead of using the money to pay for something, you’re paying yourself back. The benefit is that the lender may report your loan activity to the credit reporting agencies, helping you grow your credit history. Of course, as with regular loans, this can come with fees and interest charges, so you need to balance your credit goals with financial feasibility and needs.

Establish good credit habits

In addition to choosing a loan that works best for you, establishing consistent good credit habits is important to build a long, healthy credit history. Understanding the common credit score factors can help guide you as you make important credit decisions. Here are some of those factors and habits to keep in mind:

Make payments on time

Making on-time payments is one of the most influential credit score factors and can weigh heavily on your credit score. Set reminders or automatic payments if you know you can consistently make your payments. If you’re worried you’re going to miss a payment, contact the company as soon as possible. They may have options for customers like payment extensions. Not all companies offer accommodation in these situations, but it may benefit you to ask. If you’re worried this is going to miss several payments, ask if they have any sort of hardship plan.

Exceed minimum payments

It’s best practice to pay off your credit card balances in full each month. Making only the minimum payments on credit card balances can be costly because of high interest rates typically found on credit cards.

However, if you’re having financial difficulties, making at least the minimum payment will keep your account current and won’t count as a missed payment, which can have a significant negative impact on your credit score. Consider paying more than the minimum when you reach financial stability.

Do not max out credit limit

Your credit utilization, which measures how much of your available credit limit you’re using, is another important credit score factor. Keeping your balances as low as possible is best, but if your balances are high, a good goal is to get your balances down to less than 30% of your credit limit.

Be mindful of applying for too much credit

When you apply for certain types of credit, you may get a hard inquiry on your credit report. Hard inquiries or “new credit” can affect your credit score. Applying for several loans can send a signal that you may be taking on more debt than you can manage.

This doesn’t mean you shouldn’t apply for credit if you need it — hard inquiries are one of the least influential credit score factors and the impact they have on your credit score will lessen over time. Just be cautious about having multiple hard inquiries on your credit in a short time frame.

Review your credit report

Even if you don’t think you have a credit history, you should still check your credit reports. You can get free credit reports from each of the nationwide credit reporting agencies (TransUnion, Equifax and Experian) every week from annualcreditreport.com.

As you start and continue building your credit history, checking your reports regularly can help you stay on top of important changes and allow you to keep an eye out for identity theft. Lenders tend to provide updates to credit reporting agencies once a month, so you may not need to check every week. The important thing is to review your reports to ensure the information accurately reflects your credit history.

Credit reports may seem confusing at first, but they’re broken down into sections. TransUnion has created a credit report guide to help you understand each section and how the information in your report can impact your credit score.

Remember, building and maintaining good credit is a marathon. Good credit can’t be built successfully overnight. Keep an eye on your credit, practice smart financial habits, and you should be able to achieve the credit profile you want.