Key Takeaways:

You may not see your credit score on your credit report.

You have multiple options to receive your TransUnion® credit report and score.

There are different credit scoring models, so your score may be different depending on where you get it.

Regularly checking both your credit score and credit report will help you feel more confident managing your credit.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Credit reports and scores are so closely related, you might think that where you find one, you’ll find the other, but that isn’t always the case. If you pulled your reports looking for a score but don’t see one, you’re still on the right track. Reviewing your credit report gives you valuable insight into your credit health and can help you make sense of your credit score.

Credit score vs. credit report

Your credit report includes personal information, lists of open and closed credit accounts, credit inquiries, and public records like bankruptcies, if you have any.

Lenders often use credit reports to help them decide if they’ll approve a credit application. The information helps potential lenders understand your history of managing credit. It’s important to remember that credit reporting agencies like TransUnion don’t make lending decisions.

How your credit report relates to your credit score

Credit scores are calculated using information in your credit report. Information is added or changed from your credit report when companies, such as lenders and banks, provide updates to your account information to the credit reporting agencies. When information is added, changed or removed from your credit report, your credit score may fluctuate.

Small credit score changes may not be cause for concern, but you'll want to investigate an unexpected change. If your score drops, it’s a good idea to read your credit report to identify the reason.

Here are some reasons why your credit score can change:

| Reason for change in your score | What it means | How it can affect your score | What you can do |

|---|---|---|---|

| Credit card balance change | Your credit card balance goes up or down | Higher balances may lower your score | Try to keep credit utilization under 30%; lower is better |

| New credit applications | You apply for a new credit card or loan | A hard inquiry may cause a small, temporary score drop | Only apply for credit when needed |

| Missed or late payments | You miss a payment or pay late | Can significantly lower your score; payment history is highly influential | Set up reminders or autopay to stay on track |

| Closing out accounts | You or your lender closes a credit account | May reduce available credit and credit depth, which can impact your score | Consider keeping accounts open to maintain low utilization; keep older accounts to support credit depth |

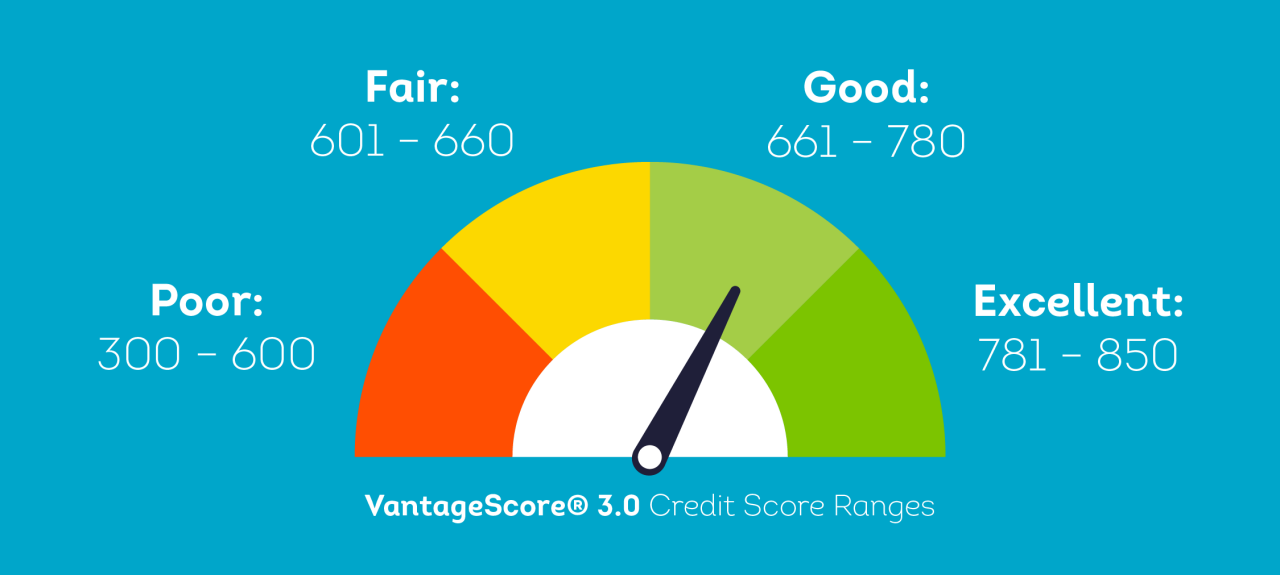

Keep in mind there are different credit scoring models. In general, credit score factors tend to overlap from model to model, but how much weight they put on those factors can vary, which is why you may have different credit scores. When assessing your credit, lenders may use a score that is different from the one that you get from TransUnion or another source. When you get a credit score from TransUnion, your credit score is calculated based on the VantageScore® 3.0 model. Lenders and insurers may use different scores to evaluate your eligibility.

If you'd like help understanding your credit report, TransUnion's credit report guide breaks down each section of your report and explains how the information may impact your credit score.

How to check your credit report

You can get your credit report for free from each of the three nationwide credit reporting agencies (TransUnion, Equifax and Experian) every week at AnnualCreditReport.com. There are other options to get your TransUnion credit report. You can learn more about ways to get your TransUnion credit report in our blog: How Do I Get My Credit Report and Score From TransUnion?

When you get your report, take a few minutes to review it to be sure all the information is accurate. If you do find anything that’s incorrect, you should dispute the errors so your credit report accurately reflects your credit history.

Pro Tip:

Checking your own credit report is considered a soft inquiry and it does not impact your credit score.

Does a credit report show your credit score?

Not all credit reports show your credit score. Some credit monitoring services, websites or apps that provide credit reports may also show a credit score as well. The free TransUnion credit report you receive from AnnualCreditReport.com doesn’t include your credit score. However, there are several ways for you can access your credit score. Credit scores are available to consumers from different sources including banks, credit unions and credit monitoring services. Each service may have different features and costs. You can purchase a one-time VantageScore® 3.0 score for $0.99 through the TransUnion Service Center.

You can get a VantageScore® credit score by TransUnion with our free credit monitoring subscription. There is no credit card required to sign up. The subscription includes daily refreshes of your TransUnion credit report.

Does everyone have a credit score?

Note that not everyone has a credit score. You can’t apply for credit on your own until you’re 18. When you apply and are approved for credit, whether it’s a credit card or another type of loan, the lender will start reporting your account activity, which includes your payment history, to credit reporting agencies. It may take several months of reporting until you’re able to receive a credit score. If you are under 18, but your parents added you as an authorized user to a credit card account, you may have a credit report already, depending on whether the account information is reported to the credit bureaus.

As you begin to build credit and accounts are added to your credit report, credit scoring models may be able to generate a credit score. Credit scores you see will typically range between 300 and 850. There is no specific starting score. Where you start depends on your personal credit history.

Healthy credit takes time

When it comes to building healthy credit, it takes a combination of time and consistent good habits.

Three tips for healthy credit:

- Make payments on time

- Keep your balances low

- Apply for credit sparingly

Develop a regular cadence for checking your credit reports. The more you check your credit reports, the more confident you’ll feel managing your credit.