Key Takeaways:

- Review your credit report thoroughly to identify any inaccurate information.

- You can dispute inaccurate information on your credit report for free online, by phone or by mail.

- Before submitting, gather any relevant documentation that can support your dispute.

- Dispute investigations typically resolve within 30 days, but can take up to 45.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Reviewing your credit report is an important part of protecting your personal information. Your credit report should be an accurate reflection of your credit history.

What information on a credit report can be disputed?

You can dispute information on credit accounts, like credit cards, mortgages and auto loans, collections and bankruptcy records, among other accounts and information.

If you see an account you don’t recognize, inaccuracies on accounts you know you’ve paid in full or old accounts that shouldn’t be on your report anymore, you can dispute those items. Some inaccuracies could be mistakes. For example, perhaps an account of a relative with a similar name, but with junior or senior, is showing on your report. Other inaccuracies could be a sign of identity theft. No matter the inaccuracy, it’s important for you to investigate.

Personal information can and should be updated as well. It’s important for lenders to have access to your current information. In the TransUnion Service Center, you can remove previous names ("AKA"), previous addresses, and employer and telephone number information. You can also select a "previous" address to be listed as your current address. If you need to add new contact information or make updates to existing personal information such as a name, address, employer, date of birth, Social Security number or address, you’ll need to send us supporting documents by mail.

Review your investigation results

You can see your active and previous disputes in the online dispute center. When our investigation is complete, we’ll send you an email to let you know, or we'll send your dispute results to you directly via postal mail. If you receive an email saying your investigation is complete, log in to review your results and updated credit report. Most dispute investigations at TransUnion are complete within two weeks, but some may take up to 30 days.

If you don’t agree with the results, it may be a good idea to contact the lender directly and provide any documentation you have to support your claim. If the lender denies your claim, it must still report to the credit agency that the information is disputed. If the lender confirms your claim, it has to tell the credit reporting agency to update or delete the item.

We don’t want an inaccuracy on your credit report to negatively impact your score and keep you from the credit opportunities you deserve. By consistently monitoring your data identity, you can help ensure your credit report shows an accurate and up-to-date picture of your credit health.

Pro Tip:

Not everything related to your credit report can be disputed. For example, you can’t dispute your credit score. Your score is calculated based on certain information in your credit report. If your score changed and you’re not sure why, you should review your credit report carefully to understand.

How to dispute something on your TransUnion credit report

Disputing your credit report is something you can do on your own – you don’t need to pay a person or service to dispute for you. Here are steps to take to dispute items on your TransUnion credit report online:

Contact your lenders

If there is something specific to one of your accounts that you don’t understand or looks wrong, it may be easier and faster to reach out to your lenders directly. You can find their contact information on your credit report. Lenders will have more details about the status of things like credit card balances and recent payments. They may be able to provide answers and resolve certain concerns quickly.

If you’re unsure if account information on your report is inaccurate or if an account balance just hasn’t been updated yet, your lender may be able to help you.

Gather supporting documents

If you have supporting documents, you should provide them to support your dispute. To help make your dispute more efficient, it may help to gather documents in advance. Examples include court or lender documents that provide specific evidence to support your claims. You can upload up to five documents for an online dispute and they should be JPG, JPEG, PDF or TIFF file types.

Currently, TransUnion doesn’t support document uploads for online public record disputes, or for updates to personal information like your Social Security number, date of birth, name or address. If you need to add or update personal information on your report, you will need to dispute by mail.

Dispute your credit report

If you’ve spotted and confirmed an inaccuracy, you can start a dispute request with the credit reporting agency. TransUnion offers a free online credit dispute service that is the quickest and easiest way to get started. If you prefer, you can also dispute by mail or phone. We also have an extensive online FAQ section there to answer your dispute-related questions.

Steps to dispute online:

- Set up a free TransUnion Service Center account if you don’t already have one. This way you can log in later to check your dispute status or view your investigation results. If you’ve requested an online dispute, freeze or fraud alert recently with TransUnion, you may already have a username and password you can use. If you’ve forgotten your username or password, the login page’s “Login Help” link will allow you to recover your account information.

- Once your account is set up or you’ve logged in, use the site navigation to access the Dispute tab and click “Start Request.” You can then choose the first item you want to dispute. When selecting an item to dispute, you’ll be taken to a new screen which will provide options for why you are disputing that item and where you can add comments to your dispute.

- If you select an account to dispute, after you provide details about that dispute, you’ll have the option to upload relevant supporting documents. If you have an identity theft report, make sure to upload it on this step. When you upload a document, there is a box you can check to note if your document relates to fraud.

- You can dispute multiple pieces of information on your credit report in the same dispute request. To include more items in your dispute or select items from other sections of your report, select “Add Another Item” to return to the full credit report. Select another item you wish to dispute and repeat the process as many times as you need before you finally submit your request. When you’ve added all the items you need to your dispute request, submit it and we’ll take it from there.

- If we can’t resolve your dispute based on what you submitted, we’ll notify your relevant lenders. They will verify the information as correct, change or delete the item and notify us. Any changes made by the lender can then be reflected on your credit report.

Review your investigation results

You can see your active and previous disputes in the TransUnion Service Center. When our investigation is complete, we’ll send you an email to let you know, or we'll send your dispute results to you directly via postal mail. If you receive an email saying your investigation is complete, log in to review your results and updated credit report. Dispute investigations at TransUnion typically resolve within 30 days, but may take up to 45 days to complete.

If you don’t agree with the results, it may be a good idea to contact the lender directly and provide any documentation you have to support your claim. If the lender denies your claim, it must still report to the credit agency that the information is disputed. If the lender confirms your claim, it must tell the credit reporting agency to update or delete the item.

Disputing fraud on your credit report

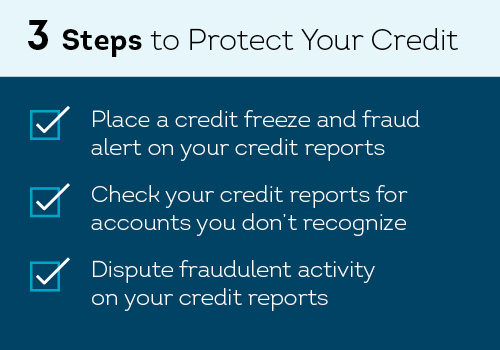

If you see an account you don’t recognize or another sign of potential fraud, it's a good idea to reach out to the company to find out more details. If they determine that someone fraudulently applied for credit in your name, they can close that account and send us a letter requesting removal of the inquiry. You can also contact us directly by mail or phone. To add a layer of protection to your credit report, you may want to add a fraud alert and credit freeze to your credit file. You can read more about fraud alerts and credit freezes in the linked blogs.

TransUnion can block the fraudulent information from your credit report. To do so, you will need to report the fraud and get an identity theft report from the Federal Trade Commission or a law enforcement agency. When submitting a dispute online, attach your identity theft report as a supporting document. When disputing by mail, include your identity theft report, a letter that identifies the fraudulent information on your credit report and proof of your identity. If acceptable, TransUnion will block the applicable items within four business days of receipt.

After you submit a dispute, TransUnion will either contact the creditor for verification or change the information directly if it does not require creditor verification. If required, once the creditor returns the verification, we will revise or delete the information in your credit report if it is inaccurate.

No change will be made if the creditor verifies its accuracy. In either case, TransUnion will send you a summary of the investigation results and, if applicable, a revised copy of your TransUnion credit report.

Do credit report disputes impact your credit score?

The act of submitting a credit report dispute does not have a direct impact on your credit score. However, if an item is changed or removed from your credit report that relates to one of the credit score factors, you may see a change in your score. How much your credit score changes depends on what type of information is changed, the credit scoring model used, and your personal credit history.

Dispute your credit report

An inaccuracy on your credit report means your credit report isn’t a true reflection of your credit history and can potentially have a negative impact on your credit health. By consistently reviewing your credit report, you can help ensure it shows an accurate and up-to-date picture of your credit history.

FAQs

Absolutely. Disputes are 100% free.

Don’t worry, there’s no impact to your credit score if you start a dispute. However, if your dispute results in items being changed or removed from your credit report, your score may change due to that.

You can dispute information on credit accounts, collections and bankruptcy records, among other accounts and information. You can find additional information on our Dispute page.

After you submit a dispute, TransUnion will either contact the creditor for verification or change the information directly if it does not require creditor verification. If required, once the creditor returns the verification, we will revise or delete the information in your credit report if it is inaccurate.

No change will be made if the creditor verifies its accuracy. In either case, TransUnion will send you a summary of the investigation results and, if applicable, a revised copy of your TransUnion credit report.