Key Takeaways:

- Soft inquiries can appear on your credit report in connection with promotional offers and account reviews.

- Soft inquiries do not impact your credit score.

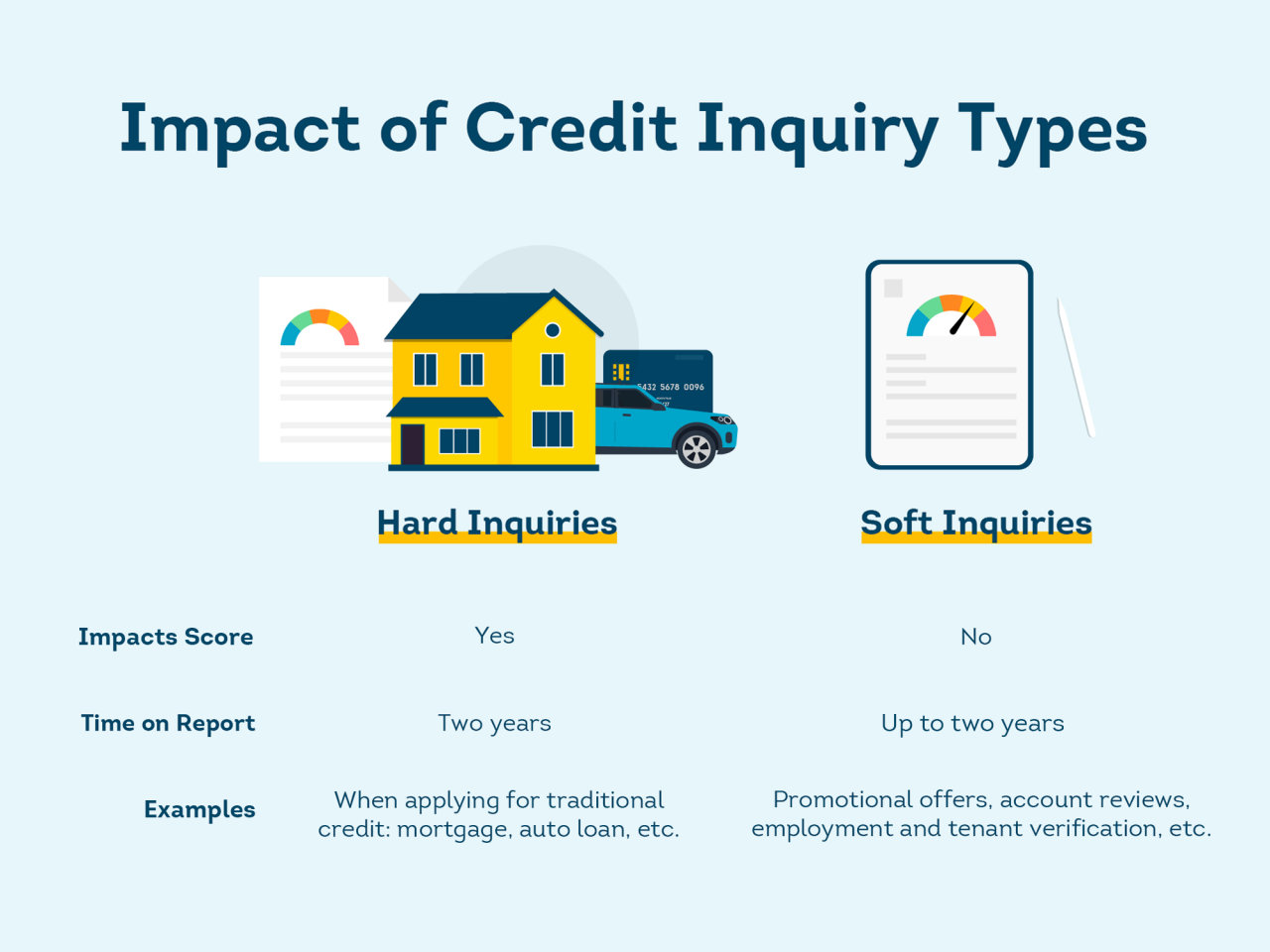

- Promotional inquiries stay on your credit report for one year, while account review inquiries can stay on your report for two years.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Your credit report is a useful tool for building and managing your financial health. As you make important financial decisions, whether it’s buying a car, applying for a credit card or searching for a new apartment, you may see the term “credit inquiry” come up as you do your research. Inquiries make up multiple sections on your credit report, so it’s important to understand what credit inquiries are and how they play a part in telling the story of your credit history.

What is a credit inquiry?

A credit inquiry is a request to review your credit report by lenders and companies that are authorized to do so. On your credit report, you’ll see hard and soft inquiries. Hard inquiries are typically associated with traditional credit applications, while soft inquiries generally appear on your credit report for non-lending purposes. Read more to learn about what soft inquiries are and when they may appear on your credit report:

Soft credit check

Soft inquiries are sometimes referred to as soft credit checks. With soft inquiries, companies receive your credit report information to make an offer of credit or as part of a review process.

There are two types of soft inquiries: promotional inquiries and account review inquiries.

Promotional inquiries

- These occur when a company wants to make a credit offer, like a pre-approved credit card or other loan offer.

- The company does not receive your full credit report.

Account review inquiries

- These can appear on your credit report when an insurer pulls your credit report for underwriting purposes, when employers verify your credit as part of their hiring process or when a landlord screens you as a potential tenant.

- A prequalification for some loans, like mortgages, can result in a soft inquiry on your credit report.

- You may also see an account review inquiry when you look at your own credit report for review.

Who can see soft inquiries on your credit report?

Only you can see all the soft inquiries on your credit report. However, users of the same product or companies in the same industry can see soft inquiries on your report associated with that product or industry. For example, insurance companies can see other insurance soft inquiries on your credit report. But those companies can’t see other types of soft inquiries.

How long does a soft inquiry stay on your credit report?

Soft inquiries can stay on your credit report for up to two years. If you see more soft inquiries on your credit report than expected, it’s not necessarily a cause for concern. These inquiries primarily appear to make you an offer of credit or reflect a review of your report unrelated to an application for credit. Having multiple soft inquiries on your credit report is not a poor reflection of your credit health.

Do inquiries affect your credit score?

Soft inquiries do not impact your credit score. Hard inquiries can have a negative impact on your credit score. Though, hard inquiries or “new credit” is one of the least influential credit score factors and the credit score impact of hard inquiries tends to lessen over time.

Hard vs. soft inquiries

When you apply for typical loans, like mortgages, auto loans and credit cards, you’ll generally see those credit checks as hard inquiries on your credit report. These are sometimes referred to as “regular inquiries.”

Hard inquiries generally stay on your credit report for two years and can impact your credit score. If you are unsure if an application will result in a hard inquiry or soft inquiry, you can ask the lender prior to applying.

Soft inquiries differ from hard inquiries in that they are associated with account reviews and promotional offers, but they don’t typically appear on your report in connection with credit applications. However, some loans, like Buy Now, Pay Later loans, only require a soft inquiry prior to approval. Unlike hard inquiries, soft inquiries do not impact your credit score.

Does a credit freeze prevent soft inquiries?

Generally, a credit freeze will not keep soft inquiries from appearing on your credit report. A credit freeze is a way to protect your credit report information and can help prevent new accounts being opened in your name.

Even if you have a credit freeze in place, lenders you currently do business with can still send targeted promotional offers and insurers can still review your credit report for underwriting purposes. You may be required to unfreeze your credit for new credit applications, rental applications and employer verifications. If you are unsure if an employment verification or rental application requires you to remove a credit freeze you have in place, you can ask the company pulling your credit report to confirm.

Monitor your credit report for inquiries

Knowing the difference between hard and soft inquiries can help you make sense of your credit report. Monitoring your credit report for important changes can help you build healthy credit. You can get your credit report for free each week from each of the three nationwide credit bureaus at annualcreditreport.com.

You can also learn about options on how to get your TransUnion credit report and score from the TransUnion credit report page.