Key Takeaways:

- A credit inquiry is a request to view your credit report by lenders and companies that are authorized to do so.

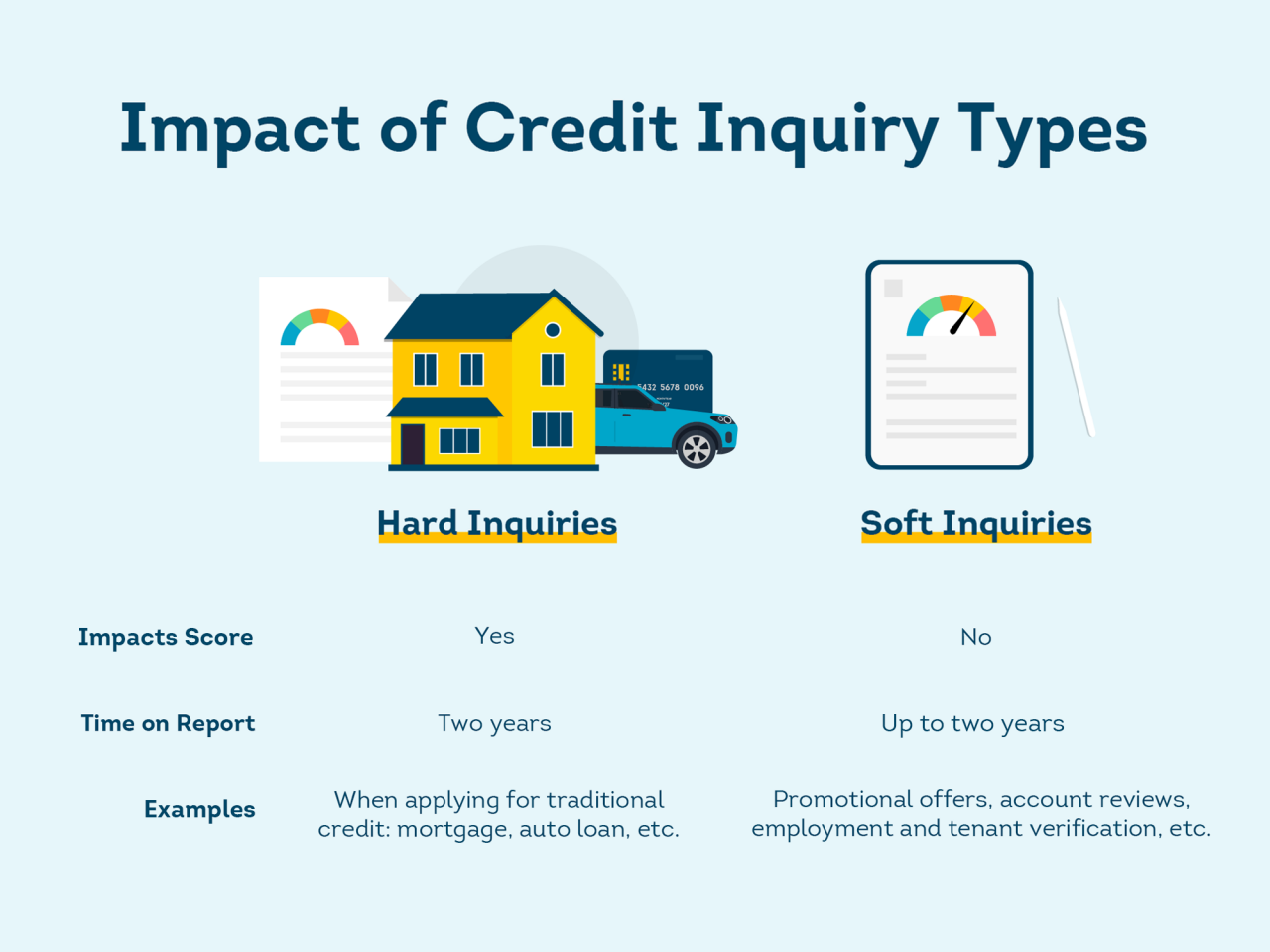

- There are two categories of inquiries: hard inquiries and soft inquiries.

- Hard inquiries, which may appear when a lender accesses your credit report as a result of a credit application, can impact your credit score.

- Soft inquiries do not impact your credit score.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

Credit inquiries, sometimes called credit checks, can appear on your credit report when a lender or company has accessed your credit report for a permissible purpose. There are different types of inquiries, usually broken down into two categories: hard and soft inquiries. Not all inquiries impact your credit score, but knowing the different types of inquiries and what they can tell you about your credit health is important.

What is a credit inquiry?

Credit inquiries indicate a lender or company has accessed your credit report with permission. Information in your credit report may be used to help lenders understand your creditworthiness when you apply for a loan. You may also see inquiries on your credit report for non-lending purposes, like when a landlord pulls your credit report or when a company wants to make an offer of credit or insurance.

Types of inquiries

Generally, credit inquiries are broken down into two categories: hard and soft inquiries.

What is a hard inquiry?

Typically, you’ll receive a hard inquiry on your credit report when you apply for a loan like a mortgage, auto loan or credit card. Loan applications could be a signal to lenders that you’re looking to take on additional debt. New credit applications are a credit score factor, so a hard inquiry may have a negative impact on your credit score. New credit is one of the least impactful credit score factors, but you should still be mindful of how often you’re applying for credit, especially ahead of major purchases like a home or car. The credit score impact of hard inquiries tends to lessen over time. Hard inquiries can stay on your credit report for up to two years.

What is a soft inquiry?

Soft inquiries don’t impact your credit score, though you should still be aware of them. Soft inquiries can stay on your credit report for up to two years. There are two types of inquiries on your TransUnion credit report: Promotional inquiries and account review inquiries.

Promotional inquiries

- Occur when a company receives limited information to make an offer of credit or insurance

- The company does not receive your full credit report

Account review inquiries

- Can appear on your credit report when an insurer pulls your credit report for underwriting purposes, employers verify your credit, or a landlord screens you as a potential tenant

- You may also see an account review inquiry if you pulled your own credit report for review

How to check your credit report for inquiries

Checking your credit report regularly will help you not only stay on top of your inquiries, but all the important information that impacts your credit health. You can obtain your credit report at annualcreditreport.com. You can learn about different options here. Depending on where you get your credit report, you may not see all soft inquiries.

Your credit report will have dedicated sections for regular inquiries (hard inquiries) and promotional and account review inquiries (soft inquiries). When you read through your regular inquiries, make sure everything looks familiar. A regular inquiry you don’t recognize could be a sign of potential fraud. It could indicate someone has access to your personal information and was able to open an account in your name. If you’re a victim of identity theft, there are multiple steps you can take to protect your credit:

- Place a credit freeze and fraud alert on your credit report

- Check your credit report for accounts you don’t recognize

- Dispute fraudulent activity on your credit report

What to do if you see an inquiry you don’t recognize

If you’re unsure about a hard inquiry, contact the company directly. Their contact information will be listed on your credit report. Sometimes an inquiry or account may seem unfamiliar because the company is using a bank you may not recognize initially. For example, store credit cards may not appear on your credit report as the store name, but rather the bank managing your account. If you see something on your credit report you believe to be inaccurate, you can dispute those items.

Inquiries and your credit

Understanding inquiries and how they appear on your credit report is one important aspect of managing your credit and protecting your important personal information. As you build your credit, continue to monitor your credit report and be mindful with credit applications so you can achieve the healthy credit you deserve.