Key Takeaways:

- Whether you should allocate your money to savings or paying off debt will depend on your financial situation.

- Paying down high interest debt is a smart thing to prioritize.

- Building an emergency savings account can help you avoid taking on debt should an unexpected expense come up.

- Creating goals and following a budget can help you get on the path to financial wellness.

Disclosure:

This post only contains educational information. No financial, tax or legal advice.

This information is for educational purposes only and we do not guarantee the accuracy or completeness of this information. This information does not constitute financial, tax or legal advice and you should consult your own professional adviser regarding your situation. This website may contain links to third party websites. We are not responsible for their content or data collection. Trademarks used in this material are property of their respective owners and no affiliation or endorsement is implied.

If you feel like debt is weighing you down, but you want to build up some savings, too, you’re not alone. Because everyone’s finances are different, when it comes to managing your savings and debt, what should be prioritized will be different for each person.

Why paying off debt is important

Money you have in a savings account will earn you money based on the interest rate, sometimes called the Annual Percentage Yield (APY). While the interest rate on your credit card, Annual Percentage Rate (APR), is the cost of borrowing money. One helps you grow money, while the other is an expense.

The interest rate for your savings account will likely be lower than those on your credit accounts, whether it’s a personal loan, credit card or other type of loan. So, the money in your savings account will typically earn less than carrying debt will cost you.

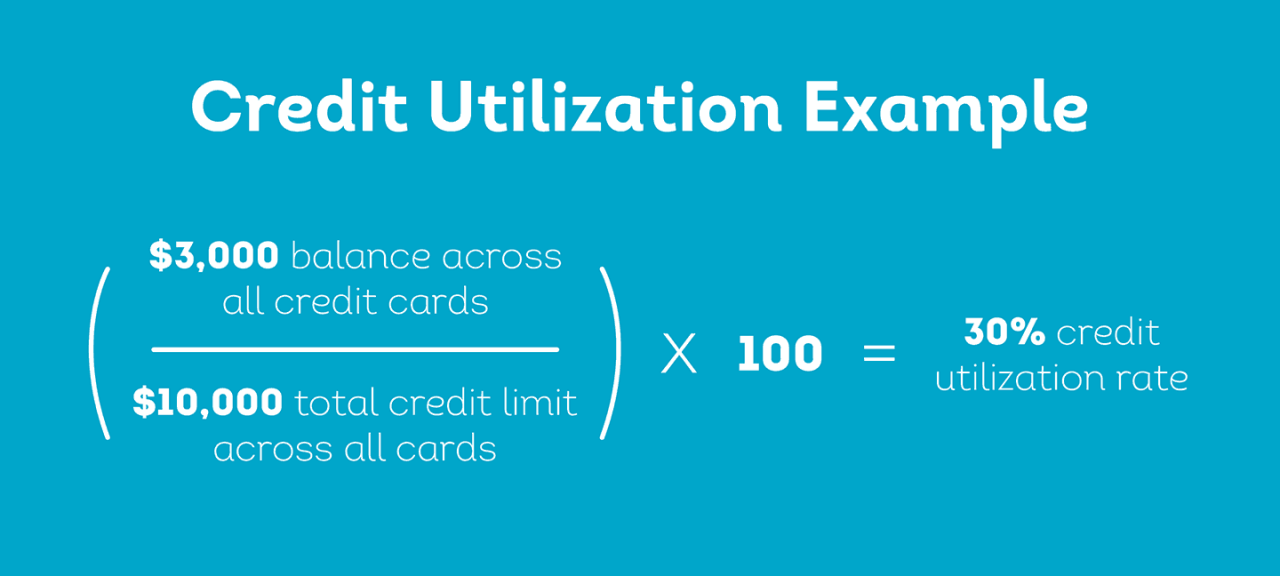

Paying down debt can also help you build healthy credit. Credit utilization, which measures how much of your available credit you’re using, is an important credit score factor. Credit utilization compares the available credit limit of your revolving accounts, like credit cards, to the combined balances you have across those accounts. If you have high balances, a good starting goal may be to get your utilization rate to 30% or lower — but the lower the better.

Why saving money is important

From a dollars-and-cents perspective, using extra cash to pay down debt is smart. However, that doesn’t mean you should ignore your savings. Saving money is important because it can prepare you for the unexpected and support your financial goals.

Putting money aside may prevent you from having to take on additional debt to cover an unexpected expense in the future, like a car or home repair or medical bills. Not only can saving money help you cover financial surprises, but building up your savings accounts can help you achieve long-term financial goals, like homeownership or retirement.

Your emergency savings account should be separate from your everyday checking account. This makes it much easier to keep track of your savings and acts as a minor barrier, so it’s less tempting to dip into it for impulse purchases.

How to pay off debt

The approach you take will depend on the type of debt you have and what your savings goals are. That’s why it’s important to approach your strategy based on your own situation.

Start by identifying exactly how much debt you have. If you’re having trouble keeping track of all your credit accounts, reviewing your credit report can be an easy way to see them all at once. In your credit report, you’ll see information like the terms, payment history and balances for each account.

Your lender will have the most up-to-date information about your accounts. For credit reporting purposes, lenders tend to provide account updates monthly, so it may take some time for the information to be updated on your report.

Pro Tip:

You can get a copy of your credit report for free each week at AnnualCreditReport.com.

For help understanding each section, we’ve created an interactive tool on how to read your credit report. Your credit report is good for seeing an overview of your credit history, but if you want to track day-to-day changes, you should check your bank or lender accounts individually.

If you have debt and are motivated to build a savings account at the same time, a balanced approach can work. Below are things to keep in mind as you make your plan.

Create a budget

You know your total debt, but there are more numbers you need to track, too. A budget can help tremendously on this journey.

You likely have a good idea what your income is, but make sure you account for all your expenses. This can help you identify any areas where you can cut back and allocate more money towards debt payments. There are many free and paid apps and services you can use to help. Your bank may even have a free tool you can use.

- Expenses to consider cutting:

- Subscriptions you’re not using

- Memberships with less expensive alternatives

- Shopping splurges

A budget can help you spot money leaks. These are small, sometimes forgotten frequent expenses that can add up over time. These could be things like bank or late fees, dining out or online shopping.

It’s easy to succumb to the urge to splurge. A good rule of thumb is to wait 24 hours before buying something new, especially if it challenges your budget. Sometimes, you may just forget that thing you walked past and don’t think about it again. After 24 hours, if you still really want it and it works for your budget, it may be worth considering.

You know your habits and needs better than anyone. While no expense should be off the table, you may not be able to cut everything. For example, cutting back on rent or transportation can be tough. Even though those may be your two biggest expenses, they are essential. So simply cutting the largest items from your budget may not always be possible. Start by considering expenses that provide the least amount of personal value to you. Some people may start by making more meals at home. Others may start with shopping expenses. Ultimately, the best choices are the ones that you will stick with.

Pro Tip:

Don’t forget free services available to you in your community. Did you know local libraries often have e-book and streaming services included with your free membership?

Prioritize your debt

Make a list of all your debts — the total amount you owe as well as the interest rate you’re paying — and place them in order based on which debt you want to start paying off more aggressively first. A common tactic is to order them based on highest interest rates first. Though, some people order their debts from lowest amounts to highest. While this may not be the best mathematically speaking, getting some quick wins can help people feel motivated to keep going.

Credit card debt considerations

Credit cards tend to have higher interest rates than other types of credit, such as a mortgage. For example, you may see credit card interest rates of 25% or higher, with mortgage interest rates less than 7%. As a result, you will likely want to prioritize paying this debt off first. It may seem more affordable to make a minimum payment rather than paying the full balance. However, because of the high interest rate, it can take a while to pay off the balance in its entirety and be expensive in the long-term.

Installment loan debt considerations

Installment loans — like mortgages, personal loans, auto loans and student loans — are a type of debt in which you pay a fixed amount for a set period of time. These usually have lower interest rates than credit cards. If your installment loan payments are manageable and you have little or no savings, it may be worth creating an emergency fund before aggressively paying these down beyond your regular monthly payments. An established emergency fund can act like a financial safety net. If you have an unexpected expense, you’ll be less likely to need to rely on a credit card or other loan to cover your bills.

One strategy to consider is refinancing your mortgage or other installment loans to a lower interest rate. It may help make payments more manageable. But note that when you refinance, you’re essentially creating a new loan, which could result in a hard inquiry on your credit report. This can have a temporary impact on your credit score.

Pro Tip:

You can use TransUnion’s mortgage calculator tool to see how your loan amount, interest rate and loan term may impact your monthly payments.

Make extra payments

The money you have from cutting back on expenses can be allocated to your debt, starting with the top of your prioritized list. If you come into extra money, like an unexpected rebate or tax refund, making extra payments can be a smart idea. Not all loans allow you to make extra payments, or they may charge a penalty for extra payments or for paying off your loan early. You can contact your lender regarding your options. Even a small amount each month can go a long way.

How to start saving money

To build your emergency savings, set a modest, achievable goal you feel comfortable with. It could be $100, $1,000 or anything between and beyond. Determine when you want to meet this goal, divide your goal amount by the number of months and set up automatic transfers to deposit it regularly. You can use the money from the expenses you cut to fund your savings.

When the goal is met, you can ramp up your debt payments even more. As your debt disappears, you can focus more on both short and long-term savings. Even if it’s a small amount, saving consistently and automatically is a great habit to establish and will pay off long term.

As you plan to save money, you may want to consider:

- Keeping your savings funds separate from your daily spending fund.

- Making your goals attainable.

- Researching different banks to see which have the best interest rates for savings accounts and terms for your goals and budget.

- Using windfalls like tax refunds and inheritances productively.

Seek help if needed

If you’re struggling to make payments, it may help to talk to your lenders about any hardship plans they may offer. Also consider getting help from a credit counselor. There are free, non-profit credit counseling organizations that can provide guidance and resources to help you manage your debt and improve your financial situation. Research several organizations to be sure they are reputable before agreeing to services.

Stick with your plan

As you determine whether to save or pay off debt — or do a little of both — know that you’re on a journey. Especially in the early stages, be sure to set achievable goals. Seeing your debt decrease and your net worth increase is a great motivator for continued success.

Be patient with yourself as you get back on track with contributing to your savings while paying down debt. You’ll find that over time, by committing to your plan you’ll reach your financial goals.

If the unexpected does happen, learn more about getting your credit back on track after a financial setback. Start with these tips on how to rebuild your credit.